In 1898:

- Congress declared war on Spain.

- The Treaty of Paris ends that same war.

- Goodyear Tire (GT) is born.

Few listed companies can trace their roots back over 100 years, let alone 123 years.

Goodyear Tire just so happens to be such a company.

The stock caught our attention when search volume amongst financial pros doubled over the weekend.

And its current valuation, a forward price to earnings (P/E) ratio of 8.51x sounds rather intriguing.

But we’re also cautious.

Shares have dropped nearly 30% from their highs and this could be one of those ‘value traps’ we’ve heard about.

So, our team took a closer look at this once great company to see if there’s still some gas left in the tank.

Goodyear Tire’s History

Based in Akron, Ohio, Goodyear Tire & Rubber Company is one of the largest tire manufacturers in the world.

Their main brands include Goodyear, Jelly, Dunlop, and soon Cooper as that acquisition closes in the second half of this year.

While the company manufactures products in 47 facilities across 21 countries, North American is still their largest geographical segment.

Their revenues breakdown as follows:

- Americas 53.2% of revenues

- Europe, Middle East, and Africa 32.2% of revenues

- Asia Pacific 14.6% of revenues

In April 2019, Goodyear entered a joint venture with Bridgestone America to form the largest tire distribution network in the U.S.

Wobbly Financials

Over the last decade, Goodyear saw revenues slip every year except one.

Why it dropped is rather interesting.

In 2010, revenues stood at $19 billion. At the end of 2019 they were down to $14.7 billion.

$2.5 billion of that move came from a stronger dollar against emerging markets.

That wasn’t the only driver.

In 2018, the company got out of Venezuela as political turmoil gripped the country.

In 2015, Goodyear dissolved a joint venture with Sumitomo Rubber, effectively exiting the motorcycle tire market.

Combined, those took off around $500 million in annual revenues.

2019 brought the U.S. China trade war took their 2% global growth in replacement tires and flat automotive production to no growth in replacement and a decline of 7% in automotive demand.

Up until 2019, Goodyear was able to deliver positive annual earnings.

2019-2020 saw a major decline in operating margins driven by the factors noted above and then Covid.

Positive Outlook

There is reason to be optimistic about the company’s future prospects.

Acquiring Cooper Tires is expected to immediately add value.

Plus, demand for new and used automobiles remains strong.

As we noted earlier, forward estimates put the price to earnings ratio at 8.51x, which is incredibly cheap all things considered.

In April 2020, Goodyear cut their dividends and amended their credit facility to ensure they remained well-capitalized.

However, Goodyear faces inflationary pressures and supply chain disruptions that will continue into the second half.

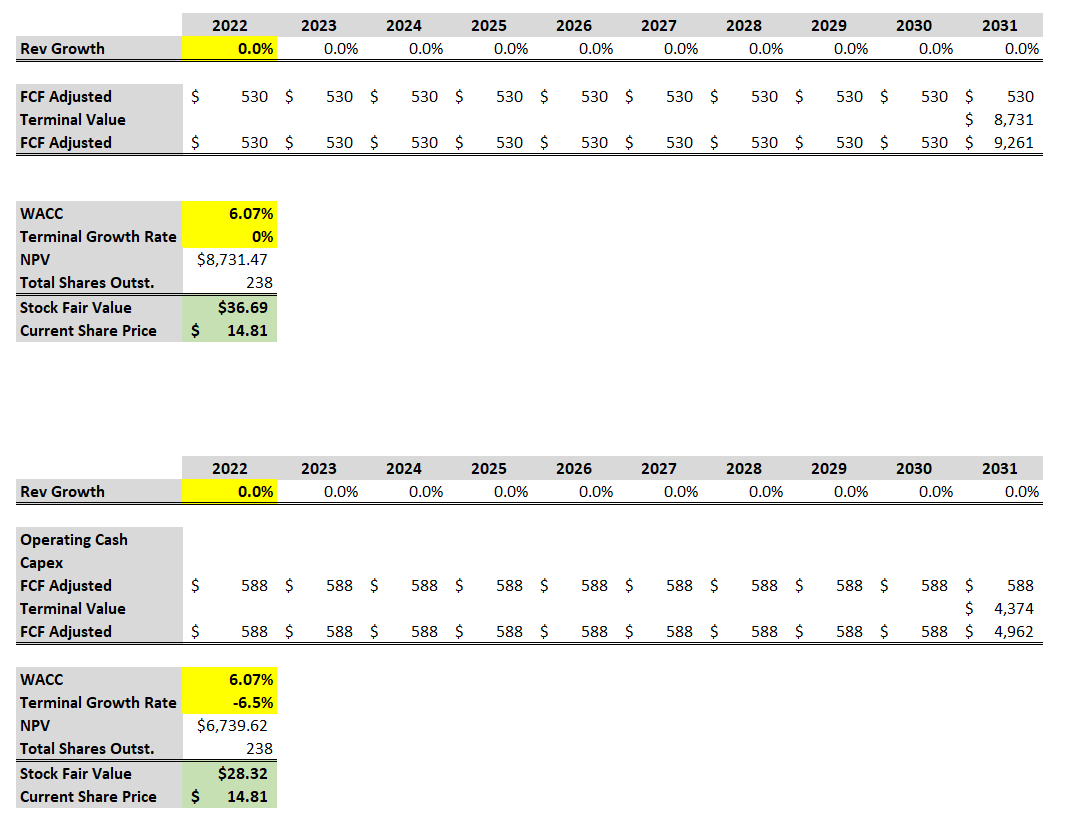

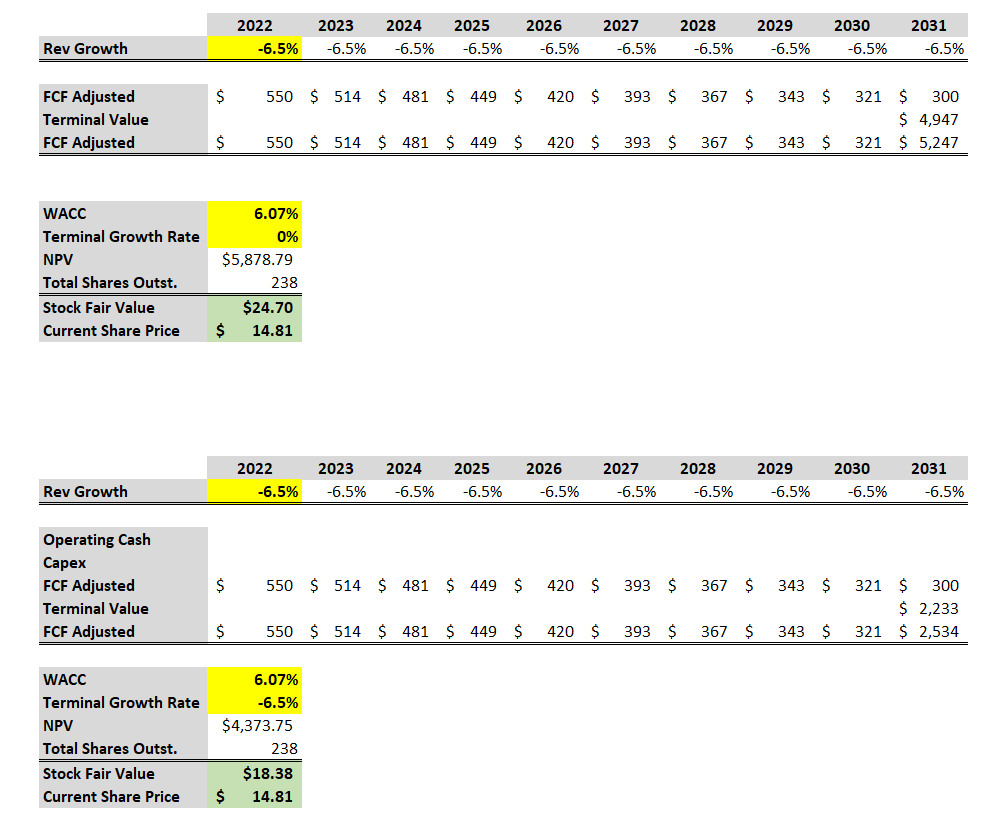

Discounted Cash Flow Analysis

We could show you all the valuation metrics that point to Goodyear Tire’s incredibly cheap price.

But all that means nothing if they can’t sustain growth.

That’s why our discounted cash flow (DCF) analysis puts a twist on our typical assumptions.

Instead of assuming growth, we want to see what declining and no growth looks like for the company based on their current free cash flow.

For this model, we’ll assume a 6.07% WACC.

We tested a 0% and a -6.5% growth rate for the 10-year period as well as a 0% and -6.5% growth rate for the terminal value.

The last model is the most intriguing.

It says that Goodyear can see cash flow declines of 6.5% every year from now until they disappear and the stock is still worth about 24% more than it is now.

What might cause this?

For starters, the company holds $6.7 billion in long-term debt.

However, if you believe the numbers in their balance sheet, the assets outweigh the liabilities.

Said differently, they could liquidate the company and pay off all their debts and still have cash left over.

Technically Speaking

For Goodyear Tire, we chose to look at a monthly chart that goes back to the early 90s.

Normally, we wouldn’t use such a long timeframe.

However, this chart highlights a fundamental story played out visually.

Shares collapsed in the mid-90s and never recovered.

Since then, it created a broad range that shares trade within – around $4.00 to $35.

Where share prices land are a function of two main items: near-term expected performance and interest rates.

As our discounted cash flow model showed, changing the growth rate can drastically affect the calculated share value.

And we know from our past work that interest rates are the same.

Our hot take

Goodyear Tire isn’t a company that will turn out 300% in a year or even five.

However, it’s a cheap stock that contains all the ingredients for near-term growth.

25% might not seem like a lot. But considering it’s the conservative model in our analysis, Goodyear presents a nice risk reward payoff.

Top-trending tickers, market-moving news alerts: Straight in your inbox!

See the pulse of the market as researched by Wall Street Elites and receive top-trending tickers and other market intelligence to inform your trades.Sign up for Wall Street Connected – our free daily newsletter that leverages our TrackstarIQ Data.