- Cheap debt and Covid fears fueled excess borrowing.

- Companies now look to deploy cash in future investments, dividends, acquisitions, and share buybacks.

- Too much cash on hand means a company doesn’t know what to do with it.

- We explain why companies that generate high Free Cash Flows (FCF) relative to their share price are more attractive and list a few examples.

$6.84 trillion.

That’s how much cash non-financial companies carried on their balance sheets at the end of Q2.

Companies hoarded cash during the pandemic to protect themselves.

As restrictions eased and the economy improved, businesses began putting that money to work.

How companies spend cash

Companies spend cash in four ways:

- Internal Investments – Purchasing equipment, adding staff, or developing new products as a means of growth.

- Acquisitions – Tapping into growth by purchasing another company.

- Dividends – Paying out cash to your shareholders.

- Share buybacks – Buying shares on the open market to reduce the total available. That means the profits are larger per share going forward.

Ideally, we want companies to invest in their future, whether through expansion or acquisition.

These days, acquisitions seem to be the soup du jour.

Sometimes those investments aren’t available or cost too much. That’s when companies turn to dividends and share buybacks.

Tax Note: Taxes paid on dividends vs. capital gains, both short-term (<year) and long-term (>year) can vary wildly based on your income and the type of account holding the stock.

Share buybacks tend to be the most common these days. Ironically, buying back stock at record highs is the worst time to do it.

Bad Cash

Not all cash is created equal.

Many companies issue debt to pay dividends.

This is fairly common in companies that pay hefty dividends like utility stocks.

However, it comes with risk.

A company can issue debt and pay dividends without a way to pay it back.

10 years later, your debt comes due. The problem is you don’t have the cash to pay it all back because you spent it on dividends.

Instead, you issue new debt. However, now rates are higher, and it costs you 5%.

Now, your cash isn’t enough to cover the interest payments. Soon, you go belly up.

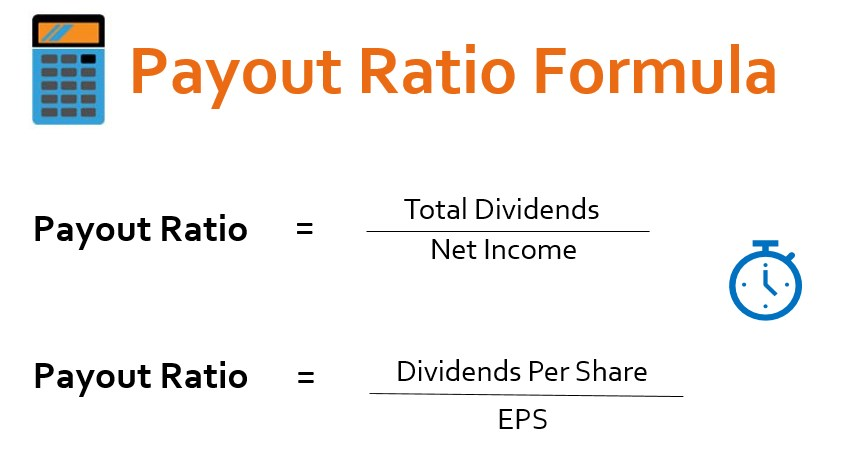

That’s why investors commonly look at the Payout Ratio.

The Payout Ratio takes your net income and divides it by the dividend payouts.

Ideally, you want your payout ratio below 100%, which means the company makes more than it pays out.

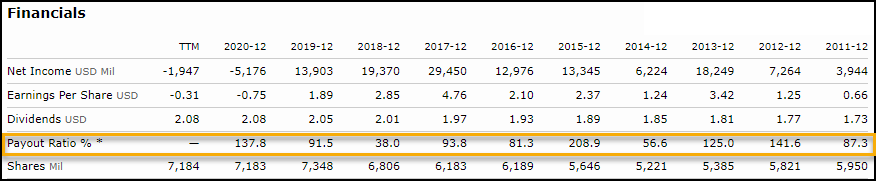

Bears criticized AT&T (T) for years because their payout ratio exceeded 100%.

Here’s a quick look at AT&T’s payout ratio over the last decade.

AT&T waffled between higher and lower payout ratios. However, with constant income growth, they never got in any real trouble.

Fun Fact: Investors relied so much on AT&T’s dividend that when they announced plans to cut their dividend in half back in May, shares plummeted over 12% in a day.

Biggest Cash Cows

Typically, we don’t like to see too much cash on the books. That indicates a company can’t figure out where to deploy capital.

One of our favorite metrics to look at is Free Cash Flow (FCF) to price.

Free Cash Flow tells us how much cash a company generates after investing in factories and expansions but before they pay dividends.

Comparing that to the price tells us how much we’re paying for that cash.

Apple (AAPL) is a great benchmark. The company is broadly owned and provides a healthy amount of cash.

Its price to FCF is 30.15x.

Here are stocks with low P/FCF ratios:

- Signet Jewelers (SIG) P/FCF = 2.41x

- Because the jewelry chain constantly changes inventory, their net income can swing from a profit to a loss some years without impacting cash flow.

- Ford Motor (F) P/FCF = 3.27x

- Surprisingly, the Detroit automotive powerhouse generates an enormous amount of free cash flow each year. While it can slip from time to time, Ford tends to have one of the best metrics out there.

- Dick’s Sporting Goods (DKS) P/FCF = 4.34x

- Dick’s has seen free cash flow grow every year except 3 in the past decade. However, they took an enormous leap in 2021 with free cash flow jumping from $187 million to $1.329 billion

A Word of Caution

Free cash flow can change rapidly when a company makes huge investments for the first time in years, such as a factory.

You should be suspect when net cash makes a huge jump from one year to the next, as it did with Dick’s. There can be a valid reason.

As an investor, you need to decide whether that will continue or was a one-off occurrence.