|

Proprietary Data Insights Top Big Bank Stock Searches This Month

|

|||||||||||||||||||||

|

Last week, we used the surge in homebuilder stocks over the last few months to help illustrate a broader contention: that the worst, which wasn’t even that bad, is behind the housing market. Brighter and even more expensive days lay ahead: The relatively modest drop (in housing prices) will bring some once priced-out people off the sidelines. But only the most job-secure and financially confident. They’ll look at lower rates, lower prices, and the subsequent lower monthly payments and pounce, biding their time until (they assume) they can refinance in 2024 or 2025 at much lower interest rates. This will, at the very least, construct a solid floor for housing prices (as in, they won’t crash), if not put them back on an upward trend. They’ll likely start to go back up by 2024, if not at some point in mid-to-late 2023. Today, we expand and further support this line of thinking. In fact, we’ll go all contrarian on you and the fat-cat Wall Street analysts. So scroll with us as we call a bottom and suggest a couple of recently downgraded stocks to buy. A preview: The Juice thinks there’s a lot of hyperbole and hysteria out there about housing that the facts simply don’t support. Facts we can’t see in lagging data, such as Q4 big-bank earnings reports. |

|||||||||||||||||||||

|

Housing |

2023’s Biggest Surprise: A Massive Housing Rebound

|

|

Key Takeaways:

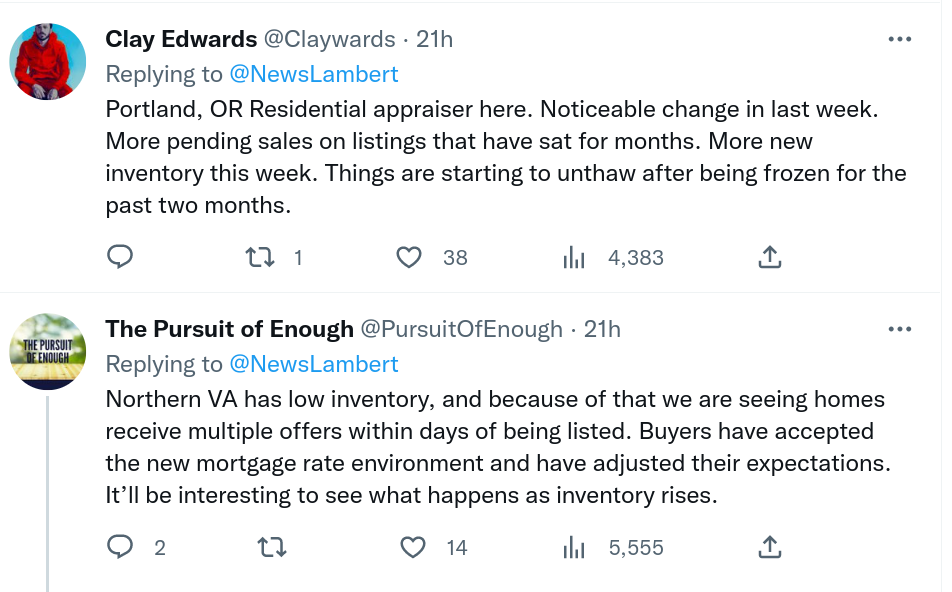

This will likely be the most image-heavy Juice yet. Because we think it’s the best way to make – and illustrate – our point that the worst is behind a housing market that will come roaring back in 2023. So follow along with us. First, there’s anecdotal evidence via on-the-ground reports from real estate agents across the country. The other day, Lance Lambert, Fortune’s excellent real estate editor, tweeted this: Source: @NewsLambert on Twitter Lambert followed up by asking real estate agents to chime in with observations from their markets. A majority of the dozens of the responses he got highlighted that in addition to the uptick in activity, we should pay attention to low supply: Source: Various Twitter users In market after market, agents are reporting low inventory, which has led to robust activity with homes staying on the market for shorter periods of time and receiving more bids. Don’t like anecdotes? Here’s some hard data from the Mortgage Bankers Association:

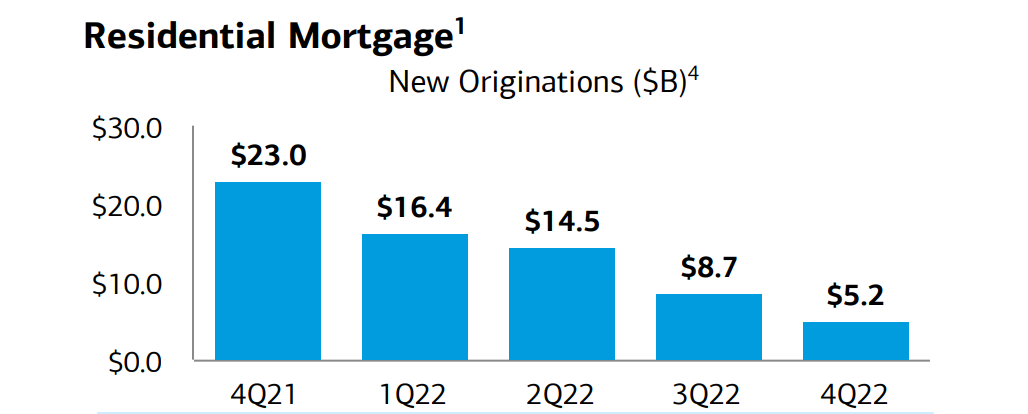

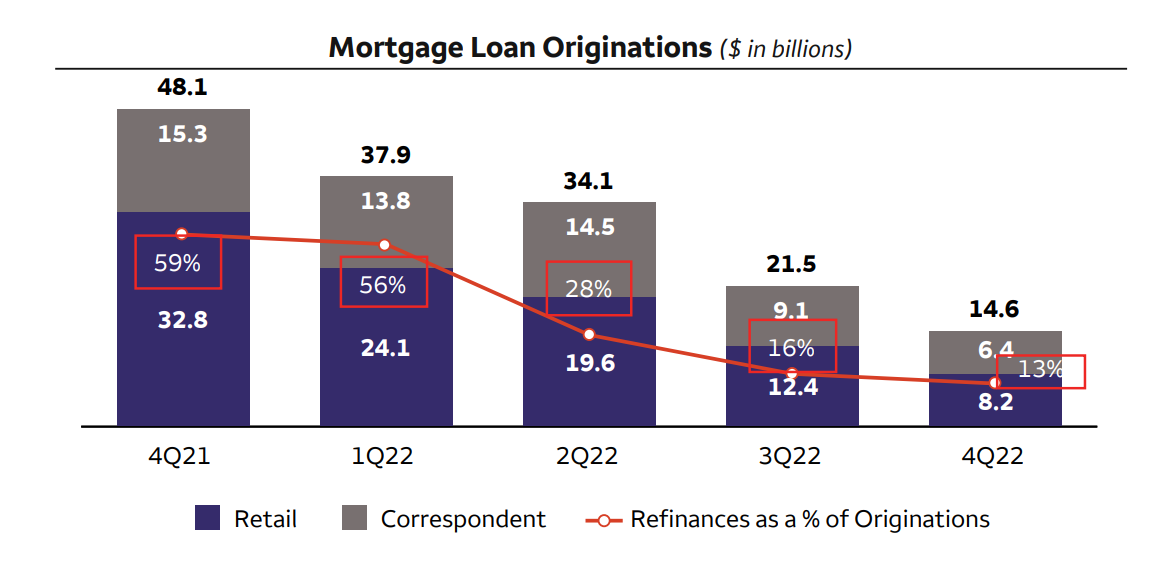

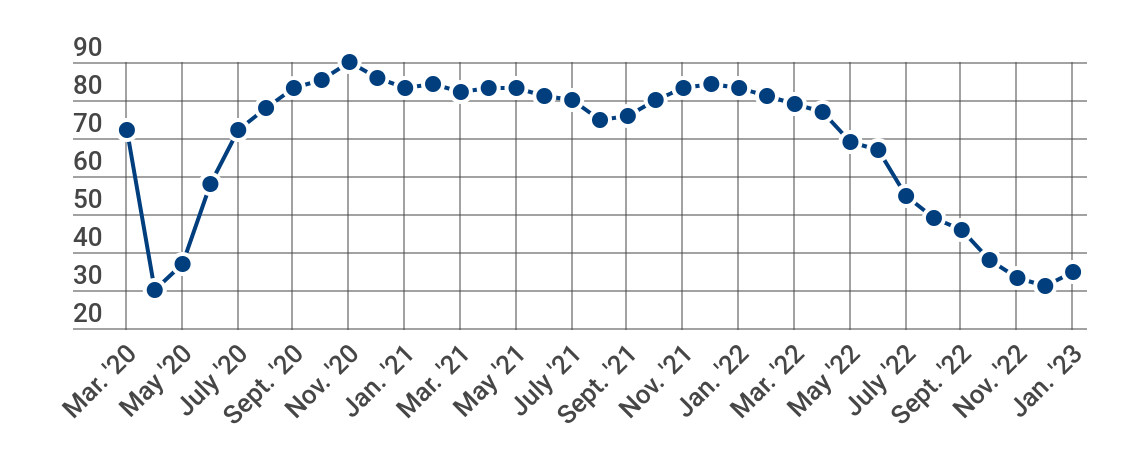

The Juice knows a trend when we see one. We also know data from the big banks often lags. Like this look at mortgage originations from Bank of America (BAC)’s recent earnings report: Source: Bank of America Similar story at Wells Fargo (WFC): Source: Wells Fargo Mortgage activity was weak in Q4 of last year. No surprise. But clearly, based on the MBA data, it’s coming back. That’s the bottom we’re calling. While these numbers might fall for another quarter, we think they’ll rebound shortly thereafter. So, after some recent analyst downgrades (the sure sign of a bottom!), we like big banks, particularly BAC and WFC. Sure, net interest income will take a hit if mortgage rates continue to come down. But refinance activity and new mortgage originations will increase, breathing life into one of the few segments that has held big banks back during this housing cooldown. Pardon that aside, but we’re not done with our theory on housing. Source: National Association of Home Builders That chart comes from the National Association of Home Builders and measures homebuilder confidence. As homebuilders cut prices to spur demand, they’re actually becoming more confident. Note the late-2022, January 2023 uptick. We have some super easy-to-read writing on the wall:

That rant made us tired. And these pretzels are making us thirsty. The Bottom Line: Fitch, a well-respected financial institution focused on credit ratings and global capital market research, predicts U.S. housing prices will be anywhere from flat to down 5% in 2023. This flies in the face of those articles you read throwing out double-digit numbers. You do you, but if you’ve been on the sidelines, you’re financially prepared, and you really want to buy a house, now might be the time to ring up your suddenly busy real estate agent. |

|

News & Insights |

Freshly Squeezed

|

|

Want to get content like this directly to your inbox? |