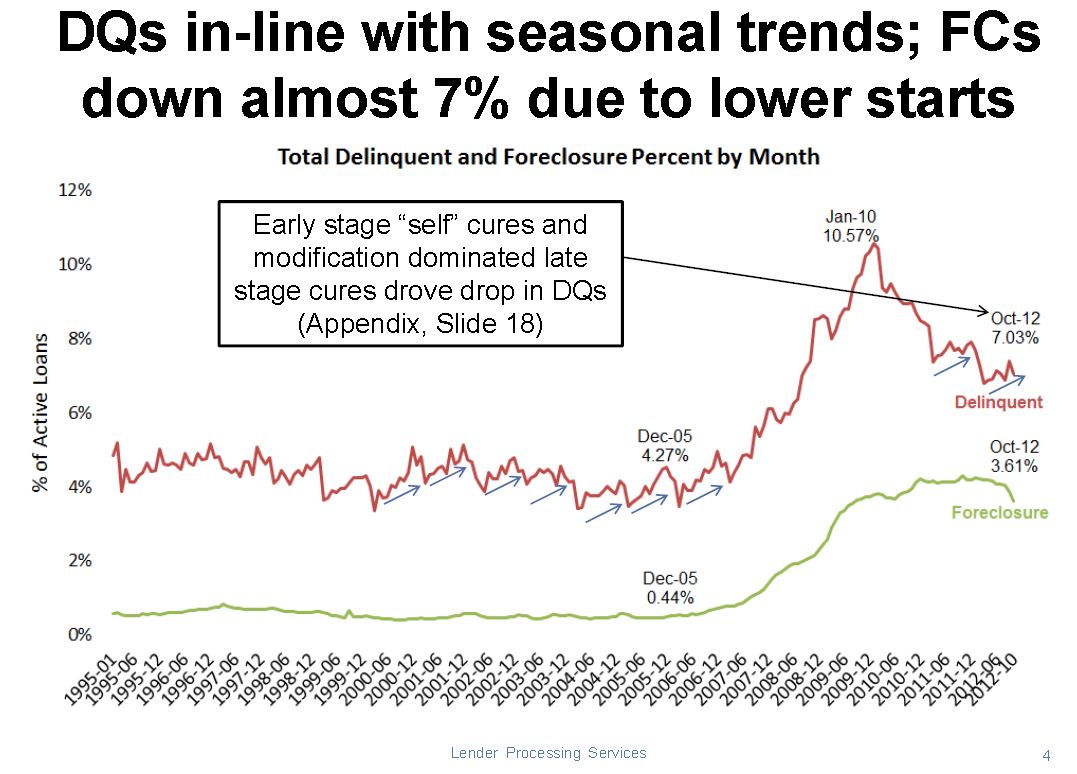

LPS released their Mortgage Monitor report for October today. According to LPS, 7.03% of mortgages were delinquent in October, down from 7.40% in September, and down from 7.58% in October 2011.

LPS reports that 3.61% of mortgages were in the foreclosure process, down from 3.87% in September, and down from 4.30% in October 2011.

This gives a total of 10.64% delinquent or in foreclosure. It breaks down as:

• 1,957,000 properties that are 30 or more days, and less than 90 days past due, but not in foreclosure.

• 1,543,000 properties that are 90 or more days delinquent, but not in foreclosure.

• 1,800,000 loans in foreclosure process.

For a total of 5,300,000 loans delinquent or in foreclosure in October. This is down from 5,640,000 last month, and down from 6,111,000 in October 2011.

This following graph shows the total delinquent and in-foreclosure rates since 1995.

Click on graph for larger image.

Click on graph for larger image.

The October Mortgage Monitor report released by Lender Processing Services (NYSE: LPS) showed a significant decline in foreclosure starts for the last two months – down 21.9 percent in October and almost 48 percent on a year-over-year basis – leading to a nearly 7 percent drop in overall foreclosure inventory. However, as LPS Applied Analytics Senior Vice President Herb Blecher explained, this fall-off in foreclosure starts is likely a temporary phenomenon, driven by new borrower notification requirements called for in the National Mortgage Settlement.

“LPS observed a drop-off in foreclosure starts in September that accelerated in October,” Blecher said. “This decline coincided with the implementation of new procedural changes outlined in the National Mortgage Settlement, which requires, among other things, that mortgage servicers provide written notice to borrowers 14 days prior to referring a delinquent loan to a foreclosure attorney. This has resulted in what is likely a temporary slowdown in foreclosure starts that we do not believe is indicative of a longer-term trend. However, we will continue to monitor this activity closely in the coming months.”

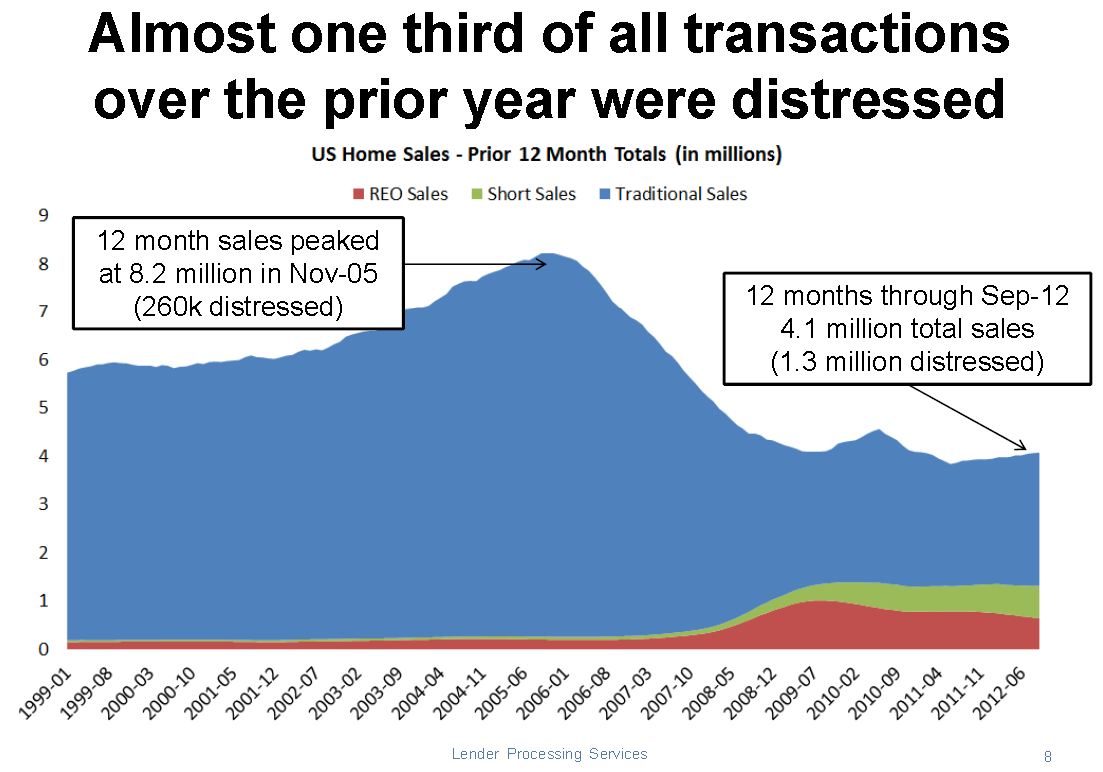

The second graph shows a break down of home sales by conventional, foreclosure and short sale.

The second graph shows a break down of home sales by conventional, foreclosure and short sale.

As the housing market slowly recovers, we’d expect distressed sales to decline and conventional sales to increase. This appears to be starting.

There is much more in the mortgage monitor.