Bruce Webb brings an interesting perspective to the current situation as pundits and politicians figure out ‘what is acceptable’ and what ‘they can live with’ her at AB and at his new website Social Security Defender: (see link below):

Scheduled vs Payable Benefits: three definitions of Solvency

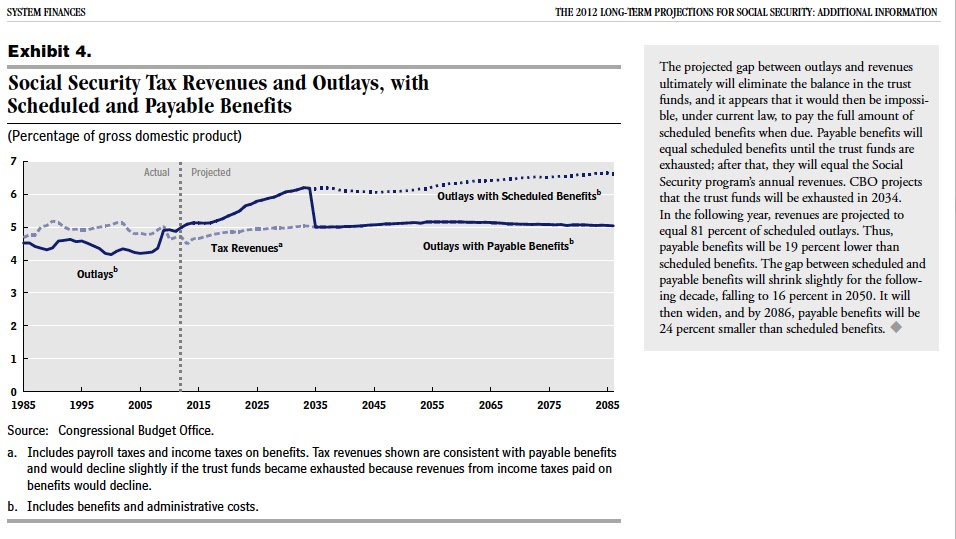

As usual click to embiggen.

When it comes to Social Security there are three definitions of ‘Solvency’, one used by the ‘Actuary’ another by the ‘Defender’ and the third by the ‘Reformer’. And it is this difference that lays at the heart of the policy disagreements on how to achieve it. Something ostensibly all three seek.

For the ‘Actuary’ ‘Solvency’ is mostly a value free concept. Social Security is solvent when all income from all sources equals all costs leaving Trust Fund assets equalling 100% of the next years projected cost. This is known as having a ‘Trust Fund Ratio’ of 100. If the Trust Funds are projected to be solvent for the upcoming 10 year window Social Security is judged to be in ‘Short Term Actuarial Balance’. If the Trust Funds are projected to maintain that solvency, or at least end up with it without going into the hole over a 75 year period it is judged to be in ‘Long Term Actuarial Balance’. And since 2003 the Trustees added an additional measure of solvency measured over the ‘Infinite Future Horizon’.

Under current law Social Security has a ‘scheduled benefit’ which is the arithmetic result of a formula calculated ultimately on the course of Real Wage increases over the worker’s lifetime. It also has a ‘payable benefit’ based on a formula that is calculated by a combination of Real Wage setting the initial benefit, inflation setting the continuing benefit, and total wages driving the income. The details are not important for the present purpose, suffice it to say that ‘scheduled benefit’ is the measure of Cost while ‘payable benefit’ is the measure of Income minus Cost. And as such ‘involvency’ represents that point here Cost exceeds Income to the extent that Trust Fund assets are driven below a TF Ratio of 100. Or in an alternative formulation when those assets are driven to zero. At which time we have a scenario as depicted in the above figure: a sudden reset of payable benefits from the schedule (where they were topped off by asset redemptions) to the new payable equal to then current income from taxation.

In percentage terms that sudden reset amounts to right on 25% of then current scheduled benefits and it is that discontinuity that defines ‘solvency crisis’. But here is where ‘defenders’ and ‘reformers’ depart.

For Social Security Defenders the crisis is one of a cut in benefits and the solution is putting in place policy that would maintain the scheduled benefit. For Social Security ‘reformers’ the crisis is more political, the risk that a reset in benefits from ‘scheduled’ to ‘payable’ will result in demands that the schedule be maintained via transfers from outside the dedicated income stream of FICA and tax on benefits. As a result the proposed solutions to this same ‘solvency crisis’ via benefit reset are diametrically opposed with defenders advocating measures to maintain current scheduled benefits while reformers see their task as reconciling future retirees to accepting then payable.

The key here, and the stopping point for this post is that either the prescription of the defender in saving scheduled or the reformer in reconciling retirees with payable will, if accomplished by appropriate changes in current law, satisfy the actuary’s test for solvency. As will outcomes in between. From a purely technocratic standpoint any set of policies that has scheduled and payable share the same ultimate projected line with no discontinuity meets the ‘solvency’ test. Meaning that each has ‘fixed’ Social Security by ‘preserving’ benefits in a ‘sustainable’ fashion. Without at any point addressing the question of whether the resulting benefits actually meet any standard of societal inequity.

Are cuts to scheduled actually the ‘Road to Catfood’ or a ‘Concession to Reality’? Well interestingly neither question has anything to do which the metric of ‘Solvency’. The question, while of course of the utmost importance in real terms, is somewhat orthogonal to discussions revolving around ‘actuarial balance’. Because from the latter perspective the ‘crisis’ IS the ‘discontinuity’ and not the real world implications thereof.

And a ‘fix’ is a ‘fix’.