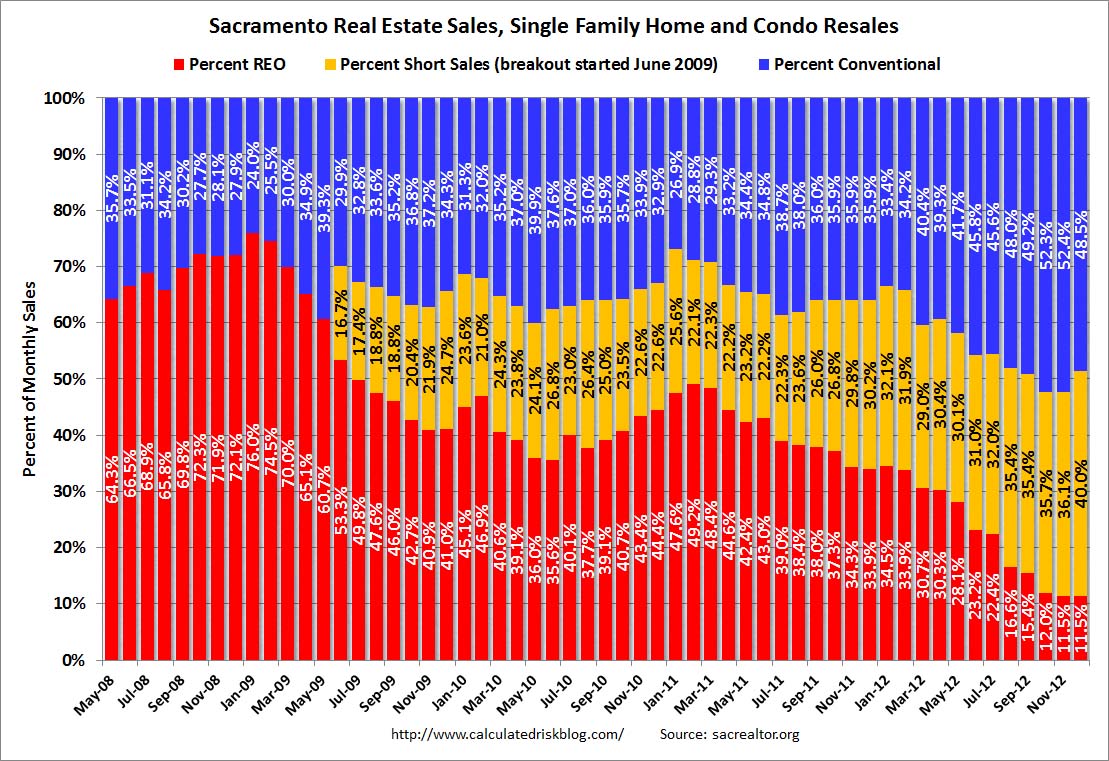

Note: I’ve been following the Sacramento market to look for changes in the mix of house sales in a distressed area over time (conventional, REOs, and short sales). The Sacramento Association of REALTORS® started breaking out REOs in May 2008, and short sales in June 2009.

Recently there has been a dramatic shift from REO to short sales, and the percentage of distressed sales has generally been declining (the percent distressed increased in December for seasonal reasons). This data would suggest some improvement in the Sacramento market.

Note on seasonal pattern: Conventional sales follow a seasonal pattern with more sales in the spring and summer than in the fall and winter. Distressed sales happen all year, so the percent of distressed sales typically increases in the winter.

In December 2012, 51.5% of all resales (single family homes and condos) were distressed sales. This was up from 47.6% last month, and down from 64.1% in December 2011. The is the lowest percentage of distressed sales for the month of December – and therefore the highest percentage of conventional sales – since the association started tracking the data.

The percentage of REOs stayed at 11.5%, the lowest since the Sacramento Realtors started tracking the data and the percentage of short sales increased to 40.0%, the highest percentage recorded.

Here are the statistics.

Click on graph for larger image.

Click on graph for larger image.

This graph shows the percent of REO sales, short sales and conventional sales.

There has been an increase in conventional sales this year, and there were almost four times as many short sales as REO sales in December (the highest recorded). The gap between short sales and REO sales is increasing.

Total sales were down from December2011, but conventional sales were up 22% compared to the same month last year. This is exactly what we expect to see in an improving distressed market – flat or even declining overall sales as distressed sales decline, but an increase in conventional sales.

Active Listing Inventory for single family homes declined 57.1% from last December.

Cash buyers accounted for 39.9% of all sales (frequently investors), and median prices were up sharply year-over-year (the mix has changed).

This seems to be moving in the right direction, although the market is still in distress. A “normal” market would be mostly blue on the graph, and this market is a long way from “normal”.

We are seeing a similar pattern in other distressed areas, with a move to more conventional sales, and a shift from REO to short sales.