Earlier:

• Summary for Week Ending March 22nd

The key reports this week are the February New Home sales report on Tuesday, Case-Shiller house prices for January, also on Tuesday, the February Personal Income and Outlays report on Friday, and the third estimate of Q4 GDP on Thursday.

Fed Chairman Ben Bernanke will speak on Monday at the London School of Economics.

Also, for manufacturing, the Dallas, Richmond and Kansas City Fed surveys for March will be released this week.

Note: the ECB deadline for Cyprus is Monday evening.

—– Monday, Mar 25th—–

8:30 AM ET: Chicago Fed National Activity Index for February. This is a composite index of other data.

10:30 AM: Dallas Fed Manufacturing Survey for March. The consensus is an increase to 3.4 from 2.2 in February (above zero is expansion).

1:15 PM: Speech by Fed Chairman Ben Bernanke, Monetary Policy and the Global Economy, At the London School of Economics and Political Science, London, United Kingdom

—– Tuesday, Mar 26th —–

8:30 AM: Durable Goods Orders for February from the Census Bureau. The consensus is for a 3.5% increase in durable goods orders.

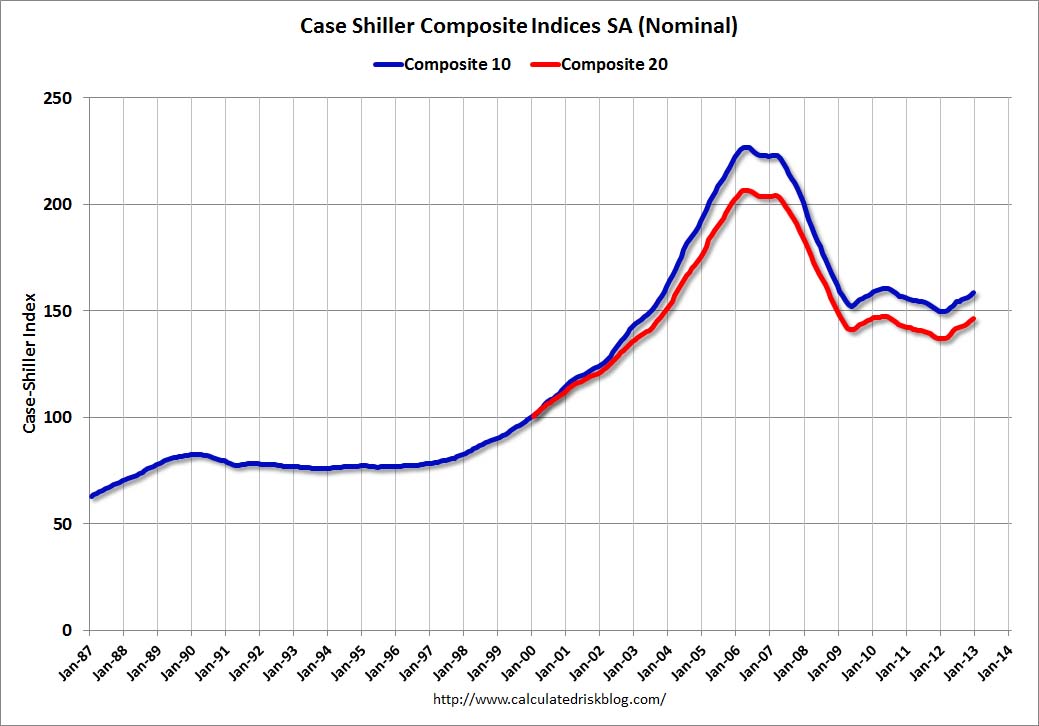

9:00 AM: S&P/Case-Shiller House Price Index for January. Although this is the January report, it is really a 3 month average of November, December and January.

9:00 AM: S&P/Case-Shiller House Price Index for January. Although this is the January report, it is really a 3 month average of November, December and January.

This graph shows the nominal seasonally adjusted Composite 10 and Composite 20 indexes through December 2012 (the Composite 20 was started in January 2000).

The consensus is for a 8.2% year-over-year increase in the Composite 20 index (NSA) for January. The Zillow forecast is for the Composite 20 to increase 8.0% year-over-year, and for prices to increase 0.8% month-to-month seasonally adjusted.

10:00 AM: New Home Sales for February from the Census Bureau.

10:00 AM: New Home Sales for February from the Census Bureau.

This graph shows New Home Sales since 1963. The dashed line is the January sales rate.

The consensus is for a decrease in sales to 425 thousand Seasonally Adjusted Annual Rate (SAAR) in February from 437 thousand in January.

10:00 AM: Richmond Fed Survey of Manufacturing Activity for March. The consensus is for a reading of 5.5 for this survey, down from 6.0 in February (Above zero is expansion).

10:00 AM: Conference Board’s consumer confidence index for March. The consensus is for the index to decrease to 69.0.

—– Wednesday, Mar 27th —–

7:00 AM: The Mortgage Bankers Association (MBA) will release the results for the mortgage purchase applications index.

10:00 AM ET: Pending Home Sales Index for February. The consensus is for a 0.7% decrease in this index.

—– Thursday, Mar 28th —–

8:30 AM: The initial weekly unemployment claims report will be released. The consensus is for claims to increase to 340 thousand from 336 thousand last week. The “sequester” budget cuts might start impacting weekly claims soon.

8:30 AM: Q4 GDP (third estimate). This is the third estimate of GDP from the BEA. The consensus is that real GDP increased 0.6% annualized in Q4, revised up from 0.1% in the second estimate.

9:45 AM: Chicago Purchasing Managers Index for March. The consensus is for a decrease to 56.1, down from 56.8 in February.

11:00 AM: Kansas City Fed regional Manufacturing Survey for March. The consensus is for a reading of minus 3, up from minus 10 in February (below zero is contraction).

SIFMA recommends 2:00 PM market close on Thursday in observance of the Good Friday Holiday.

—– Friday, Mar 29th —–

Note: Markets Closed in observance of the Good Friday Holiday.

8:30 AM ET: Personal Income and Outlays for February. The consensus is for a 0.9% increase in personal income in February (following the sharp increase in December due to some people taking income early to avoid higher taxes, and then the sharp decline in January), and for 0.6% increase in personal spending. And for the Core PCE price index to increase 0.2%.

9:55 AM: Reuter’s/University of Michigan’s Consumer sentiment index (final for March). The consensus is for a reading of 72.5.

10:00 AM: Regional and State Employment and Unemployment (Monthly) for February 2013