Black Knight Financial Services, formerly LPS, released its latest Mortgage Monitor Forecast.

Key Highlights

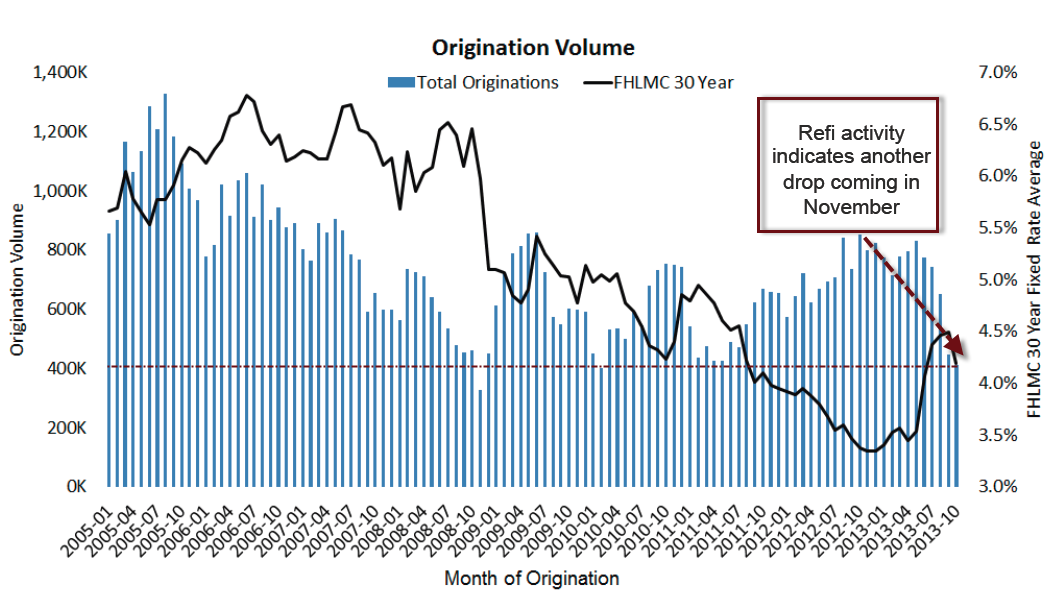

- Mortgage originations are at the lowest levels in almost four years

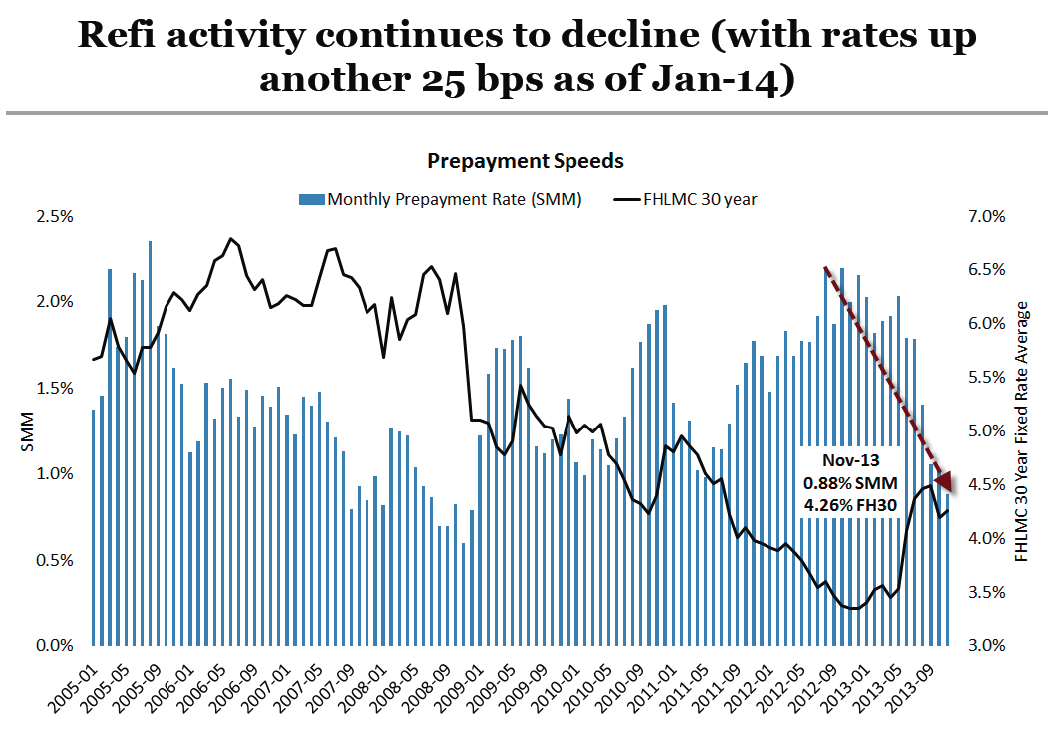

- Prepayment/refi activity indicates another drop coming

- Higher interest rates slow refinance activity

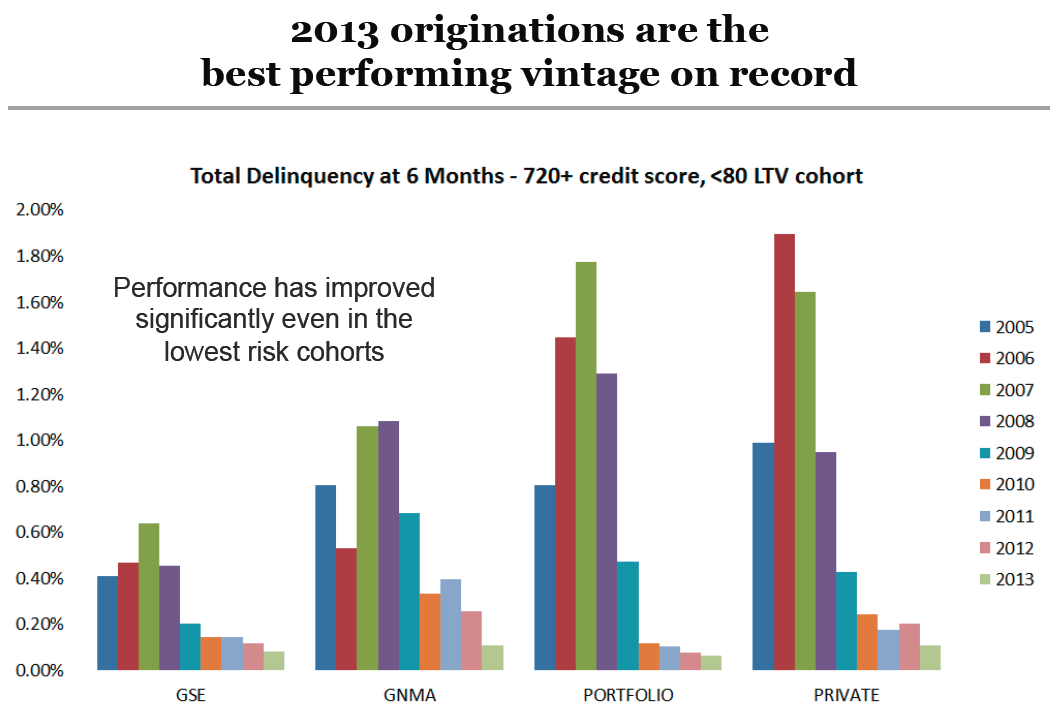

- Quality of the loans originated in 2013 have made it are the best performing vintage on on record.

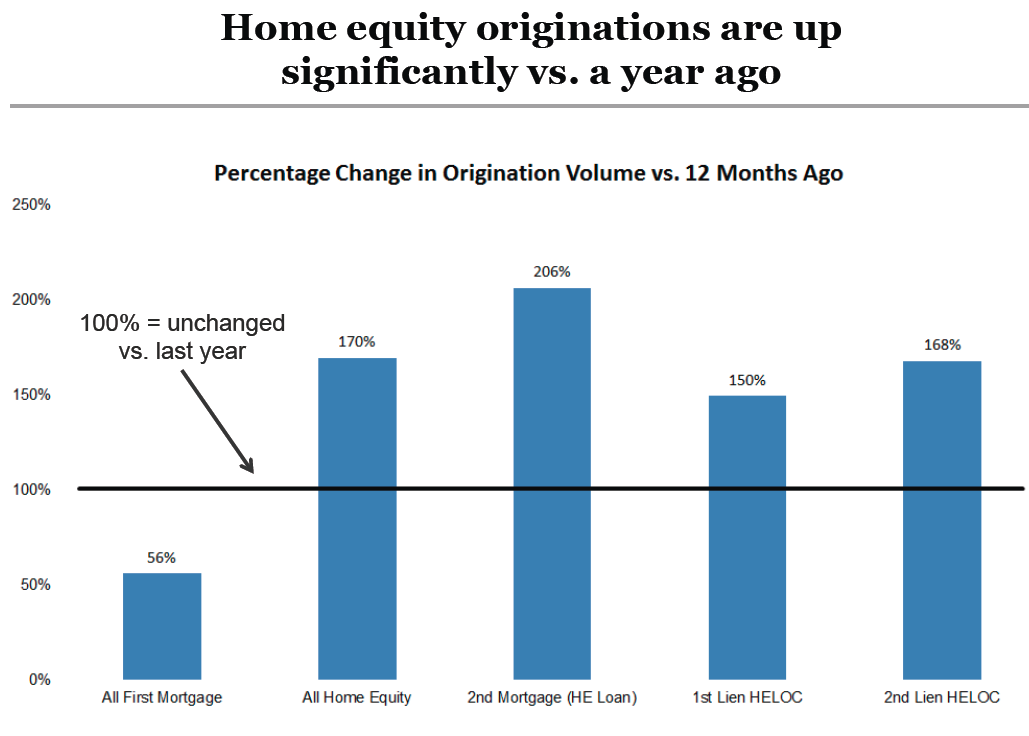

- Home equity originations are up significantly since a year ago: total HE lending is up 70%, while volume on 2nd mortgages has more than doubled

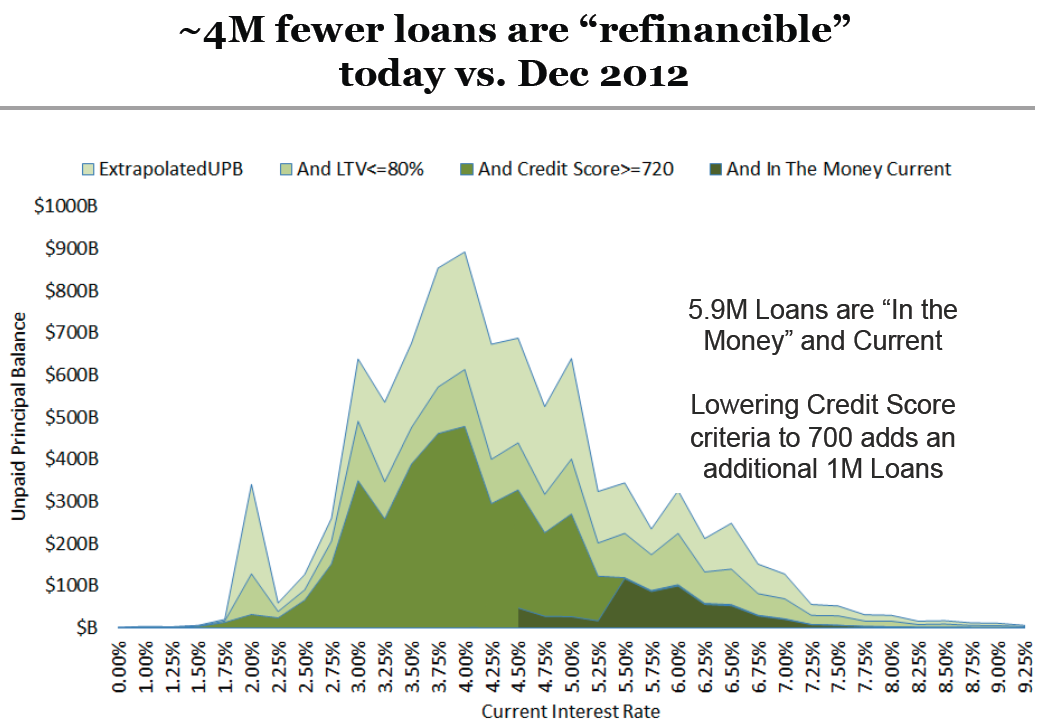

- Population of “refinancible” loans continues to shrink – Only 5.9M loans meet broadly defined criteria for refinancing, down 4M since December 2012.

- Delinquencies continue to rise among HELOCs that began amortizing

- High risk of “payment shock” in the coming three years

Here are some charts.

Anecdotes in red are mine. Click on any chart for sharper image.

Origination Volume Lowest Since 2010

Refi Activity Collapses with Rising Rates

2013 Best Vintage on Record

Home Equity Loans Up

Refinancible Loan Percentage Collapses

Payment Shock on HELOCs

Key Takeaways

Performance on 2013 origination is at record highs because of record low interest rates coupled with rising home values.

If home prices stagnate or rates continue to rise, this could be as good as it gets. The Fed is fighting major headwind battles.

Five Headwinds

- Rising rates

- Slowing economy

- Reduced values because of rising rates

- Reduce values because of rising home prices

- Demographics of retiring and downsizing baby boomers

Some may dispute point number 2.

Regardless, I think this is as good as it gets. If the economy does not slow (extremely doubtful in my opinion), rates will rise, further collapsing values.

If the economy slows, demand for housing will slow with it. This may seem circular, and it is. But it all depends on where we are in the cycle. A “recovery” since 2009 is pretty long in the tooth, historically speaking.

And even with the alleged recovery, origination are back to 2010 levels. So what happens if the recovery falters?

Values are already extremely distorted by Fed activity and all-cash purchases by the likes of Blackrock and equity funds.

Home equity extraction is likely to decline as is the stock market. Those are my opinions, but they are backed up by valuation metrics and extreme sentiment including a bubble belief the Fed can do no wrong.

Mike “Mish” Shedlock

http://globaleconomicanalysis.blogspot.com