Would you believe one fourth full ? No how about one tenth full ? How about not as dry as the Sahara desert ?

Recently I asked the question. Keynes dismissed the PIH (well before it re-emerged) as follows when discussing consumption in Chapter 8 of The General Theory …

(6) Changes in expectations of the relation between the present and the future level of income. — We must catalogue this factor for the sake of formal completeness. But, whilst it may affect considerably a particular individual’s propensity to consume, it is likely to average out for the community as a whole. Moreover, it is a matter about which there is, as a rule, too much uncertainty for it to exert much influence.

It seems to me that the very very first step in evaluating Keynes’s null is to look at the association between the ratio of consumption to current income and the ratio of future income to current income. If there is anything to the PIH it seems that it must be that a high ratio of consumption to disposable personal income must be correlated with a high ratio of future disposable personal income to current disposable personal income.

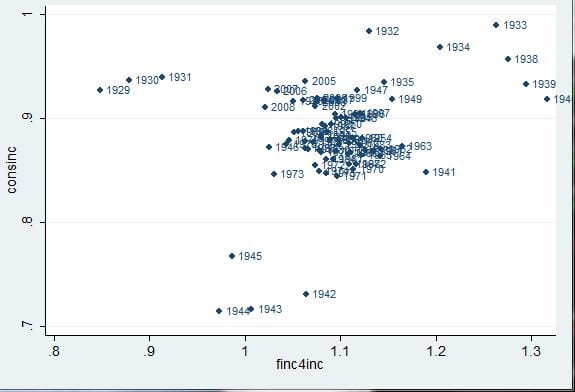

Here is a scatter of those ratios

“consinc” is the ratio of US consumption expenditures (PCECA) to US disposable personal income (A067RC1A027NBEA) both from Fred. finc4inc is the ratio of the average of US real disposable personal income (A067RX1A020NBEA) over the next four years (t+1, t+2,t+3 andt+4) to current year real disposable personal income (A067RX1A020NBEA).

The two variables should be possitively correlated if there is anything to the PIH. Now achieved future average real disposable income should be the forecast plus an error term, so the correlation should be well below one. But there is almost nothing there. the main feature of the data is that consumption was low compared to income when consumption was explicitly rationed.

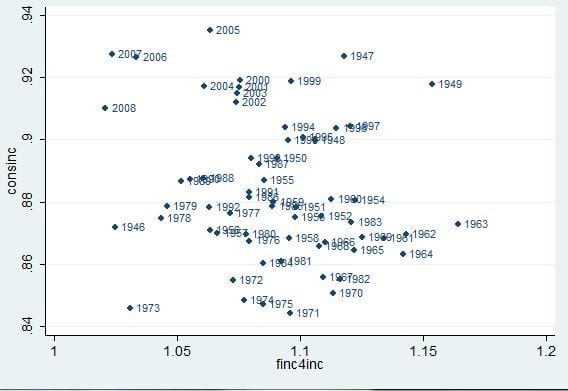

To avoid this, I also looked at data of consumption from 1946 on here

There is no pattern to explain (the correlation is actually slightly negative).

How is it possible that the profession has debated for decades how to improve on the primitive model of consumption as a function of current disposable income to consider the average agents’ consideration of future income when there is no evidence that at all ?

I will attempt to answer the question. Now there are two obvious weaknesses of my scatters. First I only consider four years into the future. Second, I ignore the real interest rate, since I don’t discount at all. Now I don’t see how one could possible argue that agents have useful insights into the distant future even if the distant future is uncorrelated with the near future, so I don’t worry at all about the first issue. The second is almost charitable with respect to the PIH. The absence of the predicted relationship between consumption and real interest rates is a well known problem with the PIH. It is clear from the scatter that the low ratio of consumption to current disposable income does not occur during periods of high achieved or predictable real interest rates (rather the opposite).

I think one important hint of an answer comes from my now eccentrically old fashioned use of disposable personal income. Theory says that consumption should depend on discounted national income minus government consumption. By using disposable income, I am assuming that consumers count current taxes as the cost of government and aren’t at all Ricardian. Also empirical work uses GNP that gross national income (or more often GDP). This doesn’t subtract depreciation of capital. There is no reason to look at gross not net income except that data on national net income weren’t available quite as soon as data on gross national income. Finally, and importantly, personal income doesn’t include income which never reaches households, that is indirect taxes (such as the employers payroll tax contributions) and undistributed profits.

Clearly consumers who own shares in firms should consider reinvested profits as adding to their wealth. There is a theoretical case for counting the government surplus and reinvested profits as part of the representative consumers income. Since profits are highly procyclical and government surpluses are too (meaning deficits are high in recessions) this makes the theoretically interesting net national product more volatile than consumption. The old fashioned and super simple assumption that consumers look at personal disposable income is an alternative explanation of the fact that consumption is less volatile than net national income.

The absolutely obvious explanation which fits the data (including the fact that consumers don’t have a clue about the sign of recent changes of the Federal budget deficit) was dismissed without consideration. The income series I used is popular among business economists who try to forecast demand (and among political scientists who try to forecast presidential elections) but it has nothing to do with the academic empirical macroeconomics literature.

Beyond that, there is the sense that to be an economist is to assume that economic agents rationally maximize under constraint.

Finally, there was a shift in Keynesian thought from 1936 to the 60s when the debate was joined. Keynes’s distinction between the consumption of individual households and aggregate consumption “whilst it may affect considerably a particular individual’s propensity to consume” seems to have been forgotten. The contrast between the time series (with consumption roughly proportional to disposable income) and the cross section (with consumption less than proportionally higher for higher income households) became a puzzle, even though the explanation was right there in The General Theory. Here I fear that later Keynesians acted as straw men (although the other case for alleged gross intellectual failure of paleo Keynesians was made entirely by lying about what they said).