Here is the Q4 report: Household Debt and Credit Report

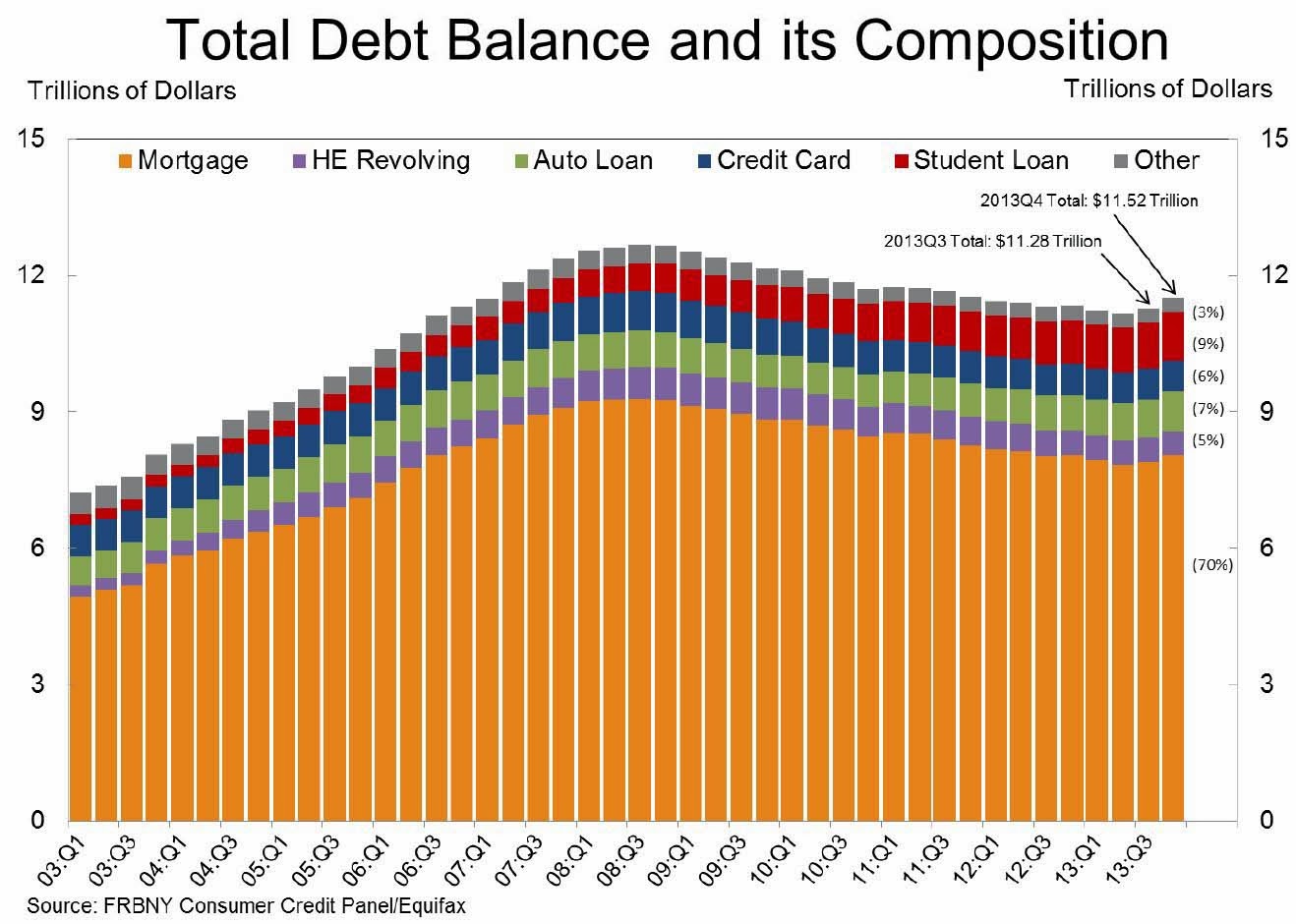

Aggregate consumer debt increased in the fourth quarter by $241 billion, the largest quarter to quarter increase seen since the third quarter of 2007. As of December 31, 2013, total consumer indebtedness was $11.52 trillion, up by 2.1% from its level in the third quarter of 2013. The four quarters ending on December 31, 2013 were the first since late 2008 to register an increase ($180 billion or 1.6%) in total debt outstanding. Nonetheless, overall consumer debt remains 9.1% below its 2008Q3 peak of $12.68 trillion.

Mortgages, the largest component of household debt, increased 1.9% during the fourth quarter of 2013. Mortgage balances shown on consumer credit reports stand at $8.05 trillion, up by $152 billion from their level in the third quarter. Furthermore, calendar year 2013 saw a net increase of $16 billion in mortgage balances, ending the four year streak of year over year declines. Balances on home equity lines of credit (HELOC) dropped by $6 billion (1.1%) and now stand at $529 billion. Non-housing debt balances increased by 3.3%, with gains of $18 billion in auto loan balances, $53 billion in student loan balances, and $11 billion in credit card balances.

emphasis added

Click on graph for larger image.

Click on graph for larger image.

Here are two graphs from the report:

The first graph shows aggregate consumer debt increased in Q4.

This suggests households (in the aggregate) may be near the end of deleveraging. If so, this is a significant change that started mid-2013.

The second graph shows the percent of debt in delinquency. The percent of delinquent debt is steadily declining, although there is still a large percent of debt 90+ days delinquent (Yellow, orange and red).

The second graph shows the percent of debt in delinquency. The percent of delinquent debt is steadily declining, although there is still a large percent of debt 90+ days delinquent (Yellow, orange and red).

From the NY Fed:

Delinquency rates improved for most loan types in 2013Q4. As of December 31, 7.1% of outstanding debt was in some stage of delinquency, compared with 7.4% in 2013Q3. About $820 billion of debt is delinquent, with $580 billion seriously delinquent (at least 90 days late or “severely derogatory”).

Delinquency transition rates for current mortgage accounts are near pre-crisis levels, with 1.48% of current mortgage balances transitioning into delinquency.

Here is the press release from the NY Fed: New York Fed Report Shows Households Adding Debt

There are a number of credit graphs at the NY Fed site.