Given stagnant wages and higher taxes, the only way households can increase spending is to go further into debt.

The New York Fed quarterly report on Household Debt and Credit shows that is what happened.

Aggregate consumer debt increased in the fourth quarter by $241 billion, the largest quarter to quarter increase seen since the third quarter of 2007. As of December 31, 2013, total consumer indebtedness was $11. 52 trillion, up by 2.1% from its level in the third quarter of 2013. The four quarters ending on December 31, 2013 were the first since late 2008 to register an increase ($180 billion or 1.6%) in total debt outstanding. Nonetheless, overall consumer debt remains 9.1 % below its 2008Q3 peak of $12.68 trillion.

Mortgages, the largest component of household debt, increased 1.9% during the fourth quarter of 2013. Mortgage balances shown on consumer credit reports stand at $8.05 trillion, up by $152 billion from their level in the third quarter. Furthermore, calendar year 2013 saw a net increase of $16 billion in mortgage balances, ending the four year streak of year over year declines. Balances on home equity lines of credit (HELOC) dropped by $6 billion (1.1%) and now stand at $529 billion. Non-housing debt balances increased by 3.3 %, with gains of $ 18 billion in auto loan balances, $53 billion in student loan balances, and $11 billion in credit card balances.

Delinquency rates improved for most loan types in 2013 Q4. As of December 31, 7.1% of outstanding debt was in some stage of delinquency, compared with 7.4% in 2013 Q3. About $820 billion of debt is delinquent, with $580 billion seriously delinquent (at least 90 days late or “severely derogatory”).

Housing Debt

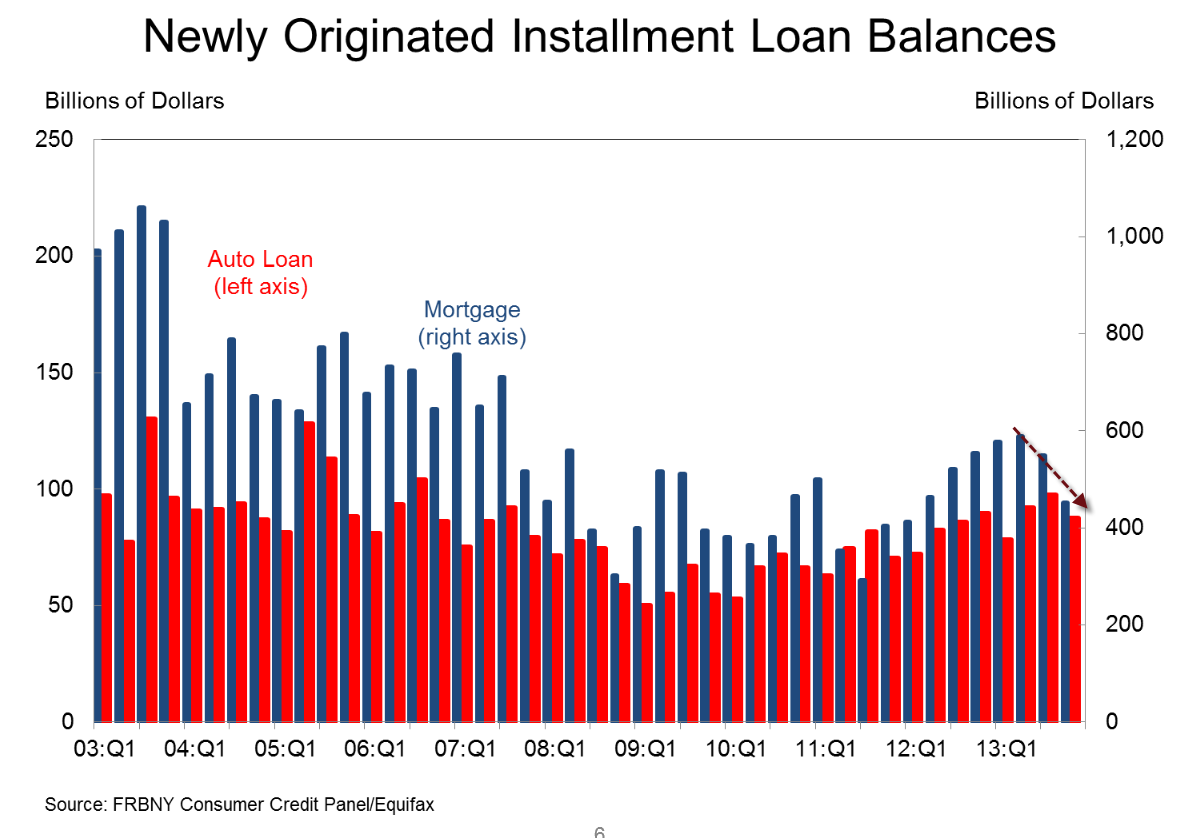

- Originations, which we measure as appearances of new mortgage balances on consumer credit reports, dropped again, to $452 billion.

- About 157,000 individuals had a new foreclosure notation added to their credit reports between October 1 and December 31.

- Foreclosures have been on a declining trend since the second quarter of 2009 and are now at the lowest levels seen since the end of 2005.

- Mortgage delinquency rates have seen consistent improvements; 3.9% of mortgage balances were 90+ days delinquent during 2013Q4, compared to 4.3% in the previous quarter.

- Serious delinquency rates on Home Equity Lines of Credit decreased to 3.2%, down from 3.5% in 2013Q3.

Student Loans and Credit Cards

- Outstanding student loan balances reported on credit reports increased to $1.08 trillion (+$53 billion) as of December 31, 2013, representing a $114 billion increase for 2013.

- About 11.5% of student loan balances are 90+ days delinquent or in default.

- Balances on credit cards accounts increased by $11 billion.

- The 90+ day delinquency rate on credit card balances increased slightly to 9.5%.

Auto Loans and Inquiries

- Auto loan originations decreased in the fourth quarter of 2013 to $88 billion.

- The percentage of auto loan debt that is 90 + days delinquent remains unchanged at 3.4%.

- The number of credit inquiries within six months – an indicator of consumer credit demand – remained virtually unchanged from the previous quarter at 169 million.

Total Debt

Quarterly and Annual Changes

Annual Changes

- Student loans accounted for $114 billion, 63.33% of the overall increase

- Auto loans accounted for $80 billion, 44.44% of the overall increase

- Combined, student loans and auto debt account for $191 billion, 107.78% of the overall increase

Quarterly Changes

- Mortgage debt accounted for $152 billion, 63.07% of the overall increase

- Student loans accounted for $53 billion, 21.99% of the overall increase

- Combined, mortgage debt and student loans account for $205 billion, 85.06% of the overall increase

Clearly fourth quarter of 2013 was a big quarter for housing, but can it last?

Auto loans had an average quarter, likely downhill from here. Trends in student debt are ominous.

Newly Originated Installment Loan Balances

Growth in auto loans and home installment loans appears to have peaked.

Delinquency Status

Percent of Delinquencies by Type

New Delinquent Balances by Loan Type

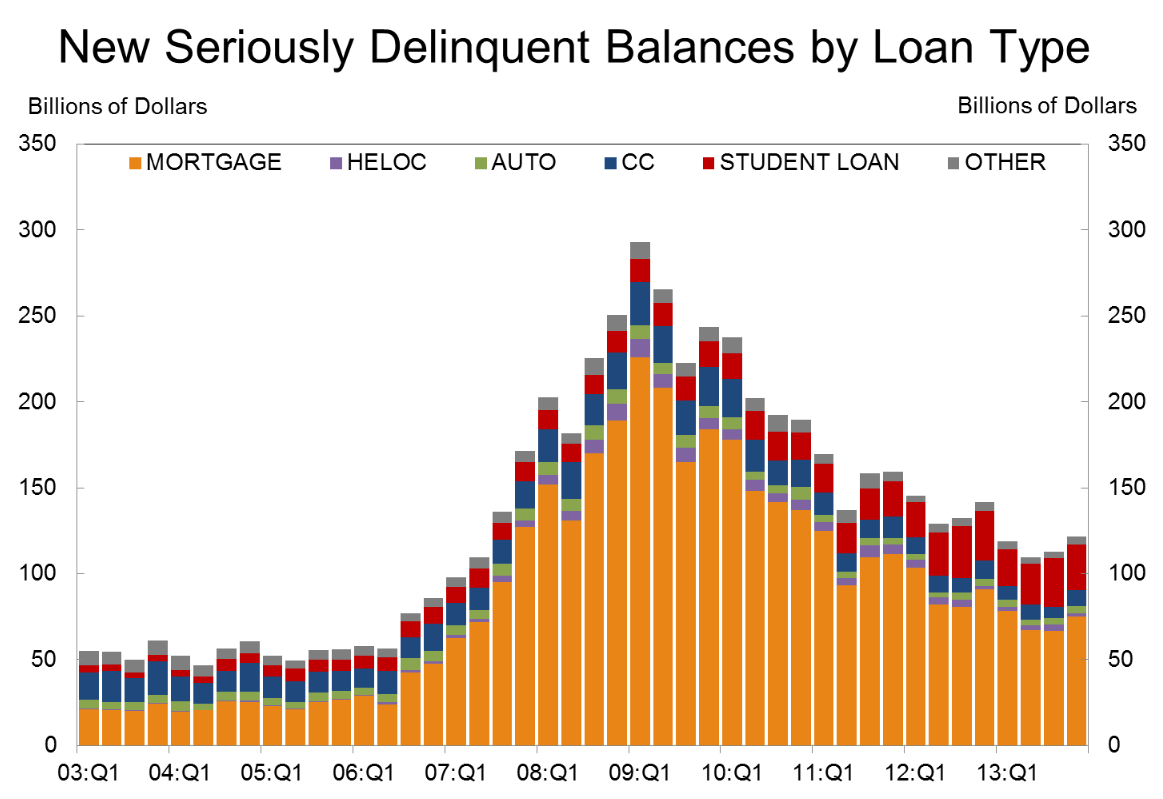

Seriously Delinquent Balances by Loan Type

There are 31 pages and many other charts in the report. Inquiring minds may wish to take a look.

Some big cracks beginning to appear? Sure looks like it.

Unless job growth and wage growth pick up, especially wage growth for the bottom half, these trends may be as good as they get given the noticeable cracks and ominous trends in student loan debt.

Mike “Mish” Shedlock

http://globaleconomicanalysis.blogspot.com