In it latest quarterly report, the BIS (Bank of International Settlements), pointed a direct finger at Fed chair Janet Yellen with an even bigger point at ECB president Mario Draghi.

Specifically, the BIS cited unthinkably low interest rates, bond market dislocations, and more taper tantrums in its Quarterly Review, December 2015, released today, Uneasy Calm Awaiting Lift-Off.

The BIS is sometimes refereed to as the central banker’s bank. Inquiring minds may with to read the “BIS About Page” for details.

Much of the BIS quarterly report is a recap of the the volatility earlier this year when the Fed signaled a potential hike in September then backed off.

Here are a few other highlights:

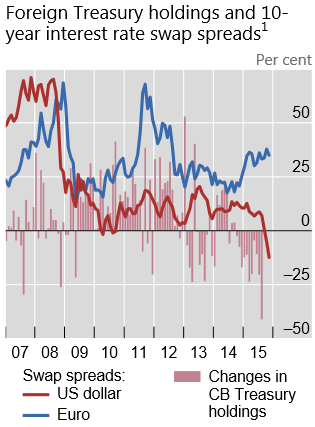

Recent Dislocations in Fixed Income Derivatives Markets

Recent quarters have witnessed unusual price relationships in fixed income markets. US dollar swap spreads (ie the difference between the rate on the fixed leg of a swap and the corresponding Treasury yield) have turned negative, moving in the opposite direction from euro swap spreads. Given that counterparties in derivatives markets, typically banks, are less creditworthy than the government, swap rates are normally higher than Treasury yields because of the additional risk premium. Hence, the negative spreads point to a possible dislocation.

Tightening in the United States May Challenge EMEs

In August 2015 the VIX had reached levels not seen since the onset of the European debt crisis

in 2011 and CDS spreads on EME sovereigns had exceeded levels experienced during the worst of

the taper tantrum. [Mish Comment: Is that the real reason for the Fed’s ultra-dovish September statement since unwound? I think so]There have also been signs that EM local currency yields are increasingly sensitive to developments in the United States. The post-crisis era has been characterised by strong international spillovers from US bond yields to emerging markets, even when those countries were at different stages of the business cycle.

And this effect seems to have strengthened over time. A simple rolling regression of an EME bond

index on US 10-year Treasury yields suggests that the potential for spillovers is larger now than it was during the taper tantrum.Tighter financial conditions may also increase financial stability risks in EMEs. Credit growth in EMEs has been strong over recent years, owing to favourable growth prospects and very easy global financial conditions. For example, the average credit-to-GDP ratio in the BRICS has rise n by close to 25% since 2010. Despite low interest rates, rising debt levels have pu shed debt service ratios for households and firms above their long-run averages, particularly since 2013, signalling increased risks of financial crises in EMEs [Mish comment: We are see a financial crisis right now in Brazil].

Debt service ratios will inevitably increase even further when lending rates start to rise. Any further appreciation of the dollar would additionally test the debt servicing capacity of EME corporates, many of which have borrowed heavily in US dollars in recent years.

“Unthinkably” Low Interest Rates

Also consider the Financial Times synopsis of the report BIS Argues for Tighter Monetary Policy in Spite of ‘Uneasy Calm’.

Central banks must not let market volatility halt their plans to retreat from crisis-fighting monetary policies, the Bank for International Settlements has warned ahead of the expected first rate rise by the US Federal Reserve in nine years.

While the current “uneasy calm” in financial markets threatened to blow up into bouts of financial turmoil, with clear tensions between markets’ behaviour and underlying economic conditions, such a threat should not dissuade monetary policymakers from taking the first steps towards tighter monetary policy, the BIS argued in its latest quarterly review.

“At some point, [the tension] will have to be resolved,” said Claudio Borio, head of the BIS’s monetary and economic department. “Markets can remain calm for much longer than we think. Until they no longer can.”

The Fed resisted raising rates this year in part because of market turmoil over the summer. Going into this month’s meeting, conditions have been milder — although the BIS noted this calm had been uneasy.

“Very much in evidence, once more, has been the perennial contrast between the hectic rhythm of markets and the slow motion of the deeper economic forces that really matter,” Mr Borio said.

The BIS has long believed that what it describes as “unthinkably” low interest rates are fuelling instability in global financial markets.

BIS Points Finger at Yellen, Draghi

I cannot find either of the above Borio quotes in the BIS article. I presume they were comments made specifically to the Financial Times.

I agree with both, especially liking “Markets can remain calm until they can’t.”

And what else can a comment about “unthinkably” low interest rates be other than a direct finger point at the key central banked involved in this mess: Fed chair Janet Yellen (previously Ben Bernanke), and ECB president Mario Draghi.

Last week, Draghi just made the apparently no longer “unthinkable” move of lowering interest rates to -0.3 percent.

For further comments on Draghi and the ECB please see …

- December 4: “No Limit” to Economic Madness.

- December 3: Euro Surges, Bonds Sink as ECB’s Rate Cut to -0.3% and Pledge of More QE Until March 2017 “or Beyond” Not Dovish Enough

Damning Indictment

It’s pretty clear the BIS knows the FED and ECB have blown major asset bubbles, but for some reason they just did not state things so clearly.

Instead the BIS speaks of “dislocations”, “unthinkables”, “uneasy calm” and how “low interest rates fuel instability.”

Yes, that’s a pretty damning indictment of central bank policy.

Mike “Mish” Shedlock