Reshoring Over Before It Ever Got Going

Recall the hype over reshoring? Manufacturing jobs supposedly were returning to the US in droves from Asia.

My view was that although some manufacturing processes returned, not many jobs came back thanks to robots and software automation. That view was far too optimistic.

Reshoring Myth and Reality

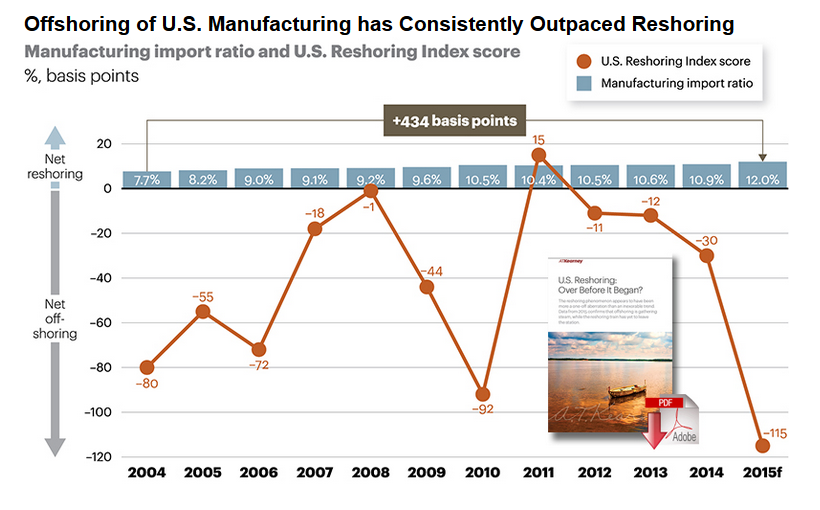

The second annual A.T. Kearney U.S. Reshoring Index shows that for the fourth consecutive year, reshoring of manufacturing operations to the United States has once again failed to keep up with offshoring.

Supply Chain reports 2015 U.S. Reshoring Index Indicates Manufacturing Reshoring Trend Has Subsided.

In 2015 the A.T. Kearney U.S. Reshoring Index dropped to -115, down from -30 in 2014, and represents the largest year-over-year decrease in the last 10 years.

Even if the effect of raw material price declines is discounted by, conservatively, holding manufacturing input values constant relative to 2014 while ignoring that same effect on the value of offshore manufactured goods, the U.S. Reshoring Index would drop to -26, still supportive of the view that the widely predicted reshoring trend seems to be over before it started.

Patrick Van den Bossche, A.T. Kearney partner and co-author of the study, stated, “The U.S. Reshoring phenomenon, once viewed by many as the leading edge of a decisive shift in global manufacturing, may actually have been just a one-off aberration. The 2015 data confirms that offshoring seems only to be gathering steam, while the U.S. reshoring train that so many predicted has yet to leave the station.”

Industries vulnerable to rising labor costs in China have been successfully relocating to other Asian countries, rather than returning to the United States. They have done so without incurring significantly higher supply chain costs, despite the weaker infrastructure and supporting ecosystems of these new low-labor-cost destinations. Vietnam has absorbed the lion’s share of China’s manufacturing outflow, especially in apparel. U.S. imports of manufactured goods from Vietnam in 2015 will be nearly triple the level of imports in 2010.

Study Findings

The A.T. Kearney U.S. Reshoring Index and the U.S. Reshoring Database provide a number of insights on the factors driving imports of offshore manufactured goods and manufacturing reshoring. Many of the report insights run counter to the points of view and “hype” regarding reshoring of manufacturing to the United States.

- Surprisingly, some of the top sectors for reshoring from 2011 to 2015 are also sectors that have led the pack in further offshoring over that same period.

- The recent increase of nearshoring to Mexico also seems to indicate that, even if U.S. companies consider leaving Asia, they may choose to stop south of the border.

- The forecast strengthening of the dollar, the oil price slide, the tightening U.S. labor market in manufacturing and the Trans-Pacific Partnership (TPP), if ratified by the U.S. Congress, will likely further weaken the case for reshoring in 2016.

- Although reshoring of manufacturing by U.S. companies is on the decline, non-U.S. companies, including Chinese companies, increasingly invest in establishing or expanding their manufacturing footprint in the United States. The insatiable U.S. consumer market, the stable political and economic environment, and the benefit of tapping into America engineering skills and manufacturing know-how are main draws.

America’s Manufacturing Renaissance Myth

Also consider The Myth of America’s Manufacturing Renaissance

For the casual observer, it is easy to get the impression that American manufacturing has entered a new and exciting period of revival.

Many in the media, along with consulting firms, think tanks, and economists, now proclaim the emergence of a U.S. “manufacturing renaissance,” marked by the “reshoring” of production and the growing competitiveness challenges of many foreign nations vis-à-vis the United States. If only this were true.

The Myth of America’s Manufacturing Renaissance: The Real State of U.S. Manufacturing, a new report by the Information Technology and Innovation Foundation (ITIF), assesses the true status of the American manufacturing economy and argues pundits have overestimated the impact of isolated incidents of reshored production and misread or ignored the data.

If there were a true renaissance, we’d expect to see growth in inflation-adjusted manufacturing value added. But in fact 2013 manufacturing value added is 3.2 percent below 2007 levels, with non-durable goods value-added (which includes chemicals and oil and gas) down almost 12 percent. U.S. manufacturers employ over a million fewer workers and there are 15,000 fewer manufacturing establishments since the beginning of the Great Recession. Moreover, America ran a $458 billion trade deficit in manufacturing goods in 2013. Hardly evidence of a renaissance.

And most of the recovery that has occurred has been cyclical in nature. In fact, 122 percent of manufacturing output growth between 2010 and 2013 was in the auto sector, whose growth is due almost solely to a rebound in U.S. consumer demand, rather than reshoring of automobile production.

“Most of the claims for a structural rebirth of U.S. manufacturing are unfortunately based on myths and anecdotes,” states Robert Atkinson, President of ITIF and co-author of the report. “Instead, any assessment of U.S. manufacturing should be based on rigorous analysis and review of the official data.”

Prevailing Wisdom

The first article, released December 21, 2015 is far more damning than the second, released January 14.

Check out the prevailing wisdom in January:

“One thing is clear – optimism about the future of U.S. manufacturing is relatively buoyant, as 68% of the executives surveyed agreed that U.S. manufacturing will experience accelerated growth in the next five years.“

A manufacturing recession has been upon us for six months.

Mike “Mish” Shedlock