Note: This index is a leading indicator primarily for new Commercial Real Estate (CRE) investment.

From the AIA: Modest Expansion for Architecture Billings Index

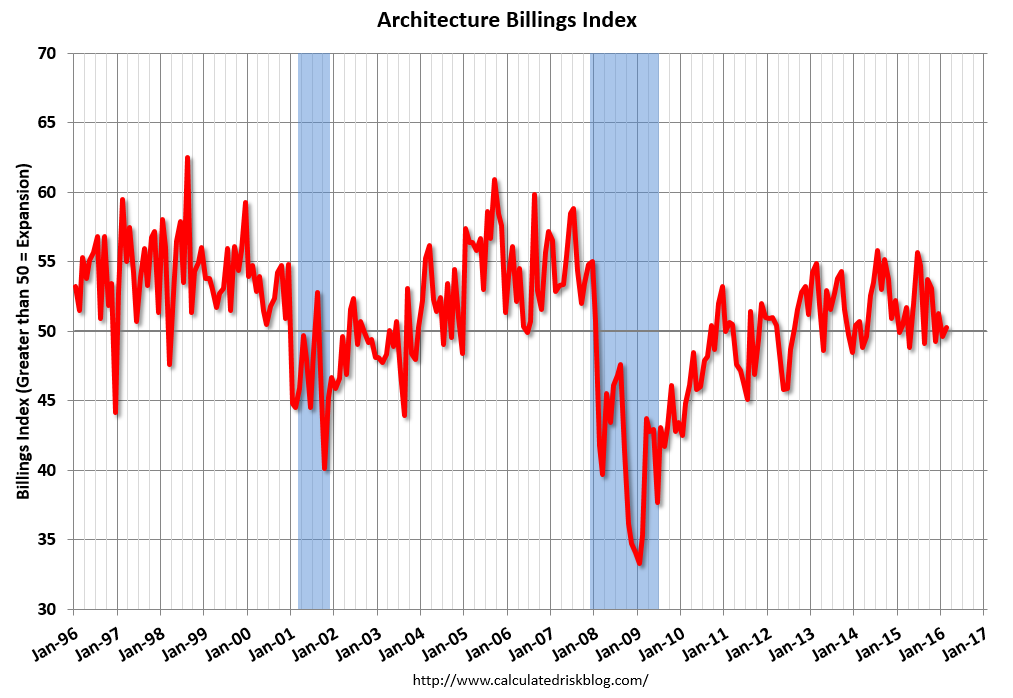

The Architecture Billings Index saw a dip into negative terrain for the first time in five months in January, but inched back up in February with a small increase in demand for design services. As a leading economic indicator of construction activity, the ABI reflects the approximate nine to twelve month lead time between architecture billings and construction spending. The American Institute of Architects (AIA) reported the February ABI score was 50.3, up slightly from the mark of 49.6 in the previous month. This score reflects a minor increase in design services (any score above 50 indicates an increase in billings). The new projects inquiry index was 59.5, up from a reading of 55.3 the previous month.

“March and April are traditionally the busiest months for architecture firms, so we should get a clearer reading of underlying momentum over the next couple of months,” said AIA Chief Economist, Kermit Baker, Hon. AIA, PhD. “Hopefully the relatively mild weather conditions recently in most parts of the country will help design and construction activity move ahead at a somewhat faster pace.”

…

• Regional averages: South (51.1), West (49.9), Northeast (49.5), Midwest (49.3)• Sector index breakdown: multi-family residential (53.0), commercial / industrial (52.3), institutional (48.1), mixed practice (47.7)

emphasis added

Click on graph for larger image.

Click on graph for larger image.

This graph shows the Architecture Billings Index since 1996. The index was at 50.3 in February, up from 49.6 in January. Anything above 50 indicates expansion in demand for architects’ services.

Note: This includes commercial and industrial facilities like hotels and office buildings, multi-family residential, as well as schools, hospitals and other institutions.

The multi-family residential market was negative for most of last year – suggesting a slowdown or less growth for apartments – but has been positive for the last five months.

According to the AIA, there is an “approximate nine to twelve month lag time between architecture billings and construction spending” on non-residential construction. This index was positive in 8 of the last 12 months, suggesting a further increase in CRE investment in 2016.