The Q3 report was released today: Household Debt and Credit Report.

From the NY Fed: Total Household Debt Remains Sluggish Yet Non-Housing Debt Continues Expanding

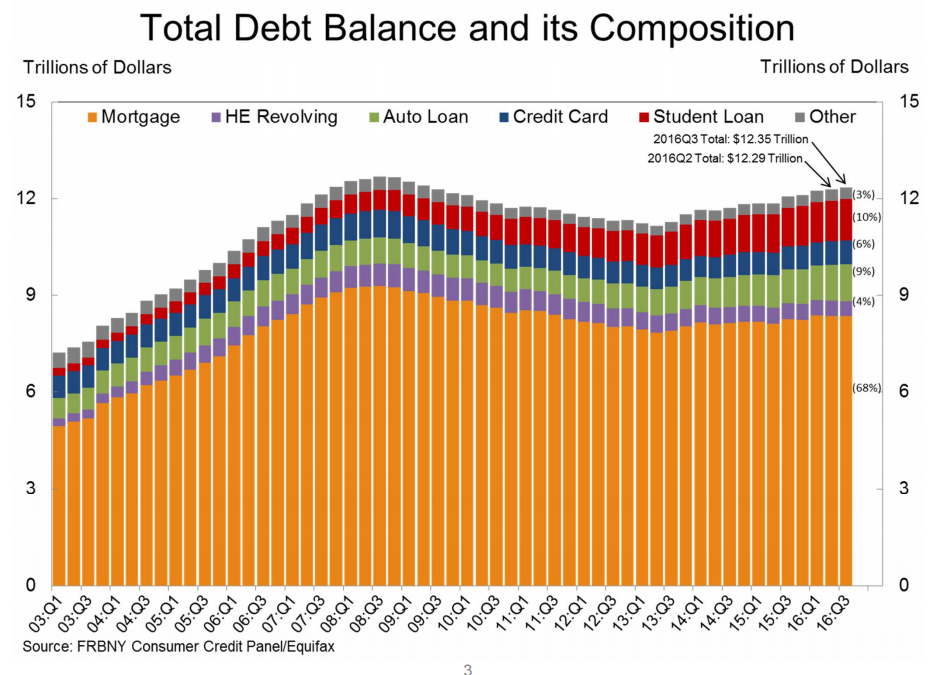

The Federal Reserve Bank of New York today issued its Quarterly Report on Household Debt and Credit, which reported that total household debt increased modestly by $63 billion (a 0.5% increase) to $12.35 trillion during the third quarter of 2016. There were increases across every type of non-housing debt, with a 2.9% increase in auto loan balances, a 2.5% increase in credit card balances, and a 1.6% percent increase in student loan balances this quarter. This report is based on data from the New York Fed’s Consumer Credit Panel, a nationally representative sample of individual- and household-level debt and credit records drawn from anonymized Equifax credit data.

…

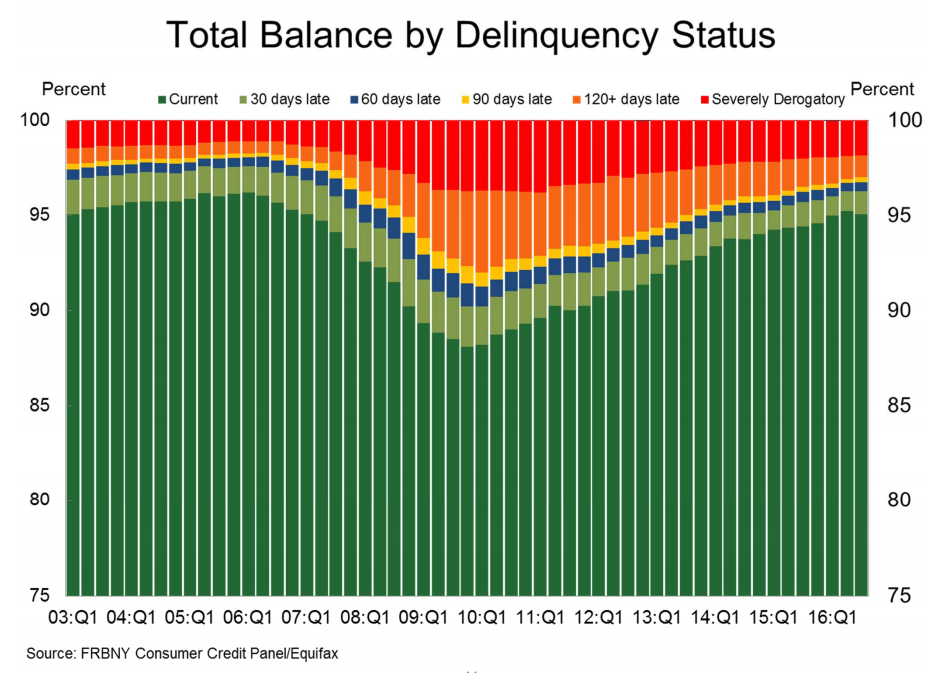

Mortgage delinquencies continued to decline as seen since the financial crisis, while new foreclosure notations reached another new low for the 18-year history of this series.

…

Overall delinquency rates worsened slightly this quarter, while the rate of bankruptcy notations continued its overall trend of improving since the financial crisis.

emphasis added

Click on graph for larger image.

Click on graph for larger image.

Here are two graphs from the report:

The first graph shows aggregate consumer debt increased in Q3. Household debt peaked in 2008, and bottomed in Q2 2013.

Mortgage debt decreased in Q3, from the NY Fed:

Mortgage balances, the largest component of household debt saw a 0.1% decline during the quarter. Mortgage balances shown on consumer credit reports on September 30 stood at $8.35 trillion, a $12 billion drop from the second quarter of 2016. Balances on home equity lines of credit (HELOC) declined by $6 billion, to $472 billion. By contrast, balances on every type of non-housing debt grew in the second quarter, boosting up the total.

The second graph shows the percent of debt in delinquency. The percent of delinquent debt is generally declining, although there was a slight increase in short term delinquencies in Q3. There is still a larger than normal percent of debt 90+ days delinquent (Yellow, orange and red).

The second graph shows the percent of debt in delinquency. The percent of delinquent debt is generally declining, although there was a slight increase in short term delinquencies in Q3. There is still a larger than normal percent of debt 90+ days delinquent (Yellow, orange and red).

The overall delinquency rate increased slightly in Q3 to 4.9%. From the NY Fed:

Overall delinquency rates worsened slightly in 2016Q3, reflecting an uptick in early delinquencies. As of September 30, 4.9% of outstanding debt was in some stage of delinquency. Of the $609 billion of debt that is delinquent, $400 billion is seriously delinquent (at least 90 days late or “severely derogatory”).