Yesterday I posted some questions for next year: Ten Economic Questions for 2017. I’ll try to add some thoughts, and maybe some predictions for each question.

7) House Prices: It appears house prices – as measured by the national repeat sales index (Case-Shiller, CoreLogic) – will be up about 6% or so in 2016. What will happen with house prices in 2017?

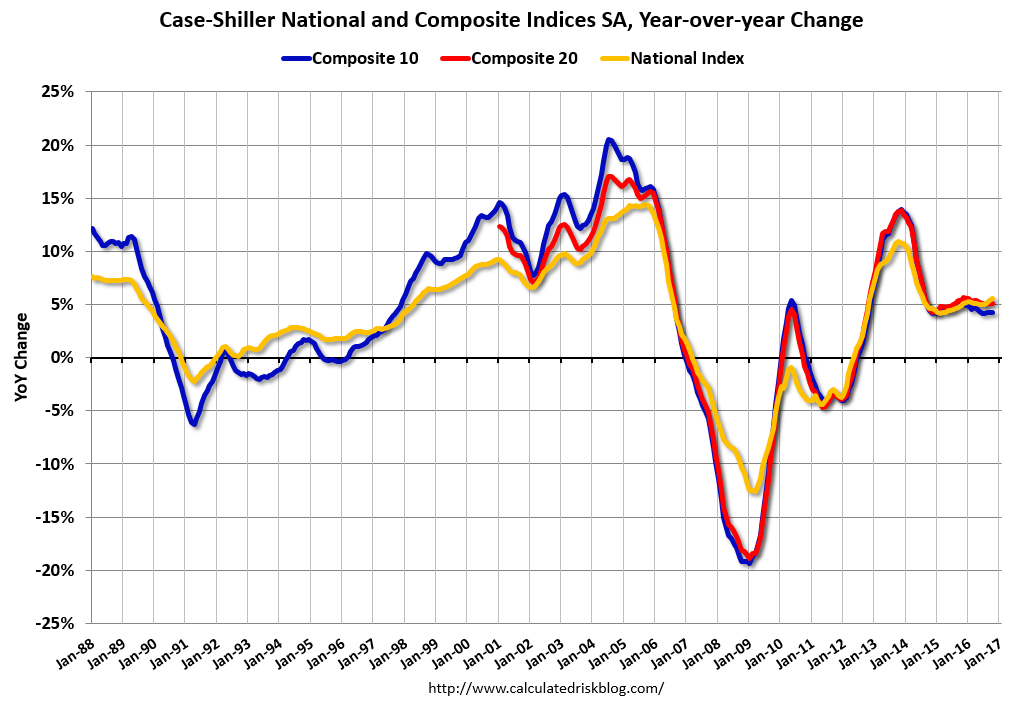

The following graph shows the year-over-year change through October 2016, in the seasonally adjusted Case-Shiller Composite 10, Composite 20 and National indices (the Composite 20 was started in January 2000).

Click on graph for larger image.

Click on graph for larger image.

The Composite 10 SA was up 4.3% compared to October 2015, the Composite 20 SA was up 5.1% and the National index SA was up 5.6% year-over-year. Other house price indexes have indicated similar gains (see table below).

Although I mostly use Case-Shiller, I also follow several other price indexes. The following table shows the year-over-year change for several house prices indexes.

| Year-over-year Change for Various House Price Indexes | ||

|---|---|---|

| Index | Through | Increase |

| Case-Shiller Comp 20 | Oct-16 | 5.1% |

| Case-Shiller National | Oct-16 | 5.6% |

| CoreLogic | Oct-16 | 6.7% |

| Zillow | Nov-16 | 6.5% |

| Black Knight | Oct-16 | 5.6% |

| FHFA Purchase Only | Oct-16 | 6.2% |

Most analysts are forecasting prices will increase in the 3% to 5% range in 2017.

Inventories will probably remain low in 2017, although I expect inventories to increase on a year-over-year basis by December of 2017. Low inventories, and a decent economy suggests further price increases in 2017.

Perhaps higher mortgage rates will slow price appreciation. If we look back at the “taper tantrum” in 2013, price appreciation slowed somewhat over the next year – but that was from a high level. In June 2013, the Case-Shiller National index was up 9.3% year-over-year. By June 2014, the index was up 6.3% year-over-year.

If inventory increases year-over-year as I expect by December 2017, it seems likely that price appreciation will slow to the low-to-mid single digits.