Notes: This CoreLogic House Price Index report is for February. The recent Case-Shiller index release was for January. The CoreLogic HPI is a three month weighted average and is not seasonally adjusted (NSA).

From CoreLogic: CoreLogic US Home Price Report Shows Prices Up 7 Percent in February 2017

Home prices nationwide, including distressed sales, increased year over year by 7 percent in February 2017 compared with February 2016 and increased month over month by 1 percent in February 2017 compared with January 2017, according to the CoreLogic HPI.

…

“Home prices and rents have risen the most in local markets with high demand and limited supply, such as Seattle, Portland and Denver,” said Dr. Frank Nothaft, chief economist for CoreLogic. “The rise in housing costs has been largest for lower-tier-priced homes. For example, from December to February in Seattle, the CoreLogic Home Price Index rose 12 percent and our single-family rent index rose 6 percent for all price tiers compared with the same period a year earlier. However, when looking at only lower-cost homes in Seattle, the price increase was 13 percent and the rent increase was 7 percent.”“Home prices continue to grow at a torrid pace so far in 2017 and these gains are likely to continue well into the future,” said Frank Martell, president and CEO of CoreLogic. “Home prices are at peak levels in many major markets and the appreciation is being driven by a number of dynamics—high demand, stronger employment, lean supplies and affordability—that will continue to play out in the coming years. The CoreLogic Home Price Index is projecting an additional 5 percent rise in home prices nationally over the next 12 months.”

emphasis added

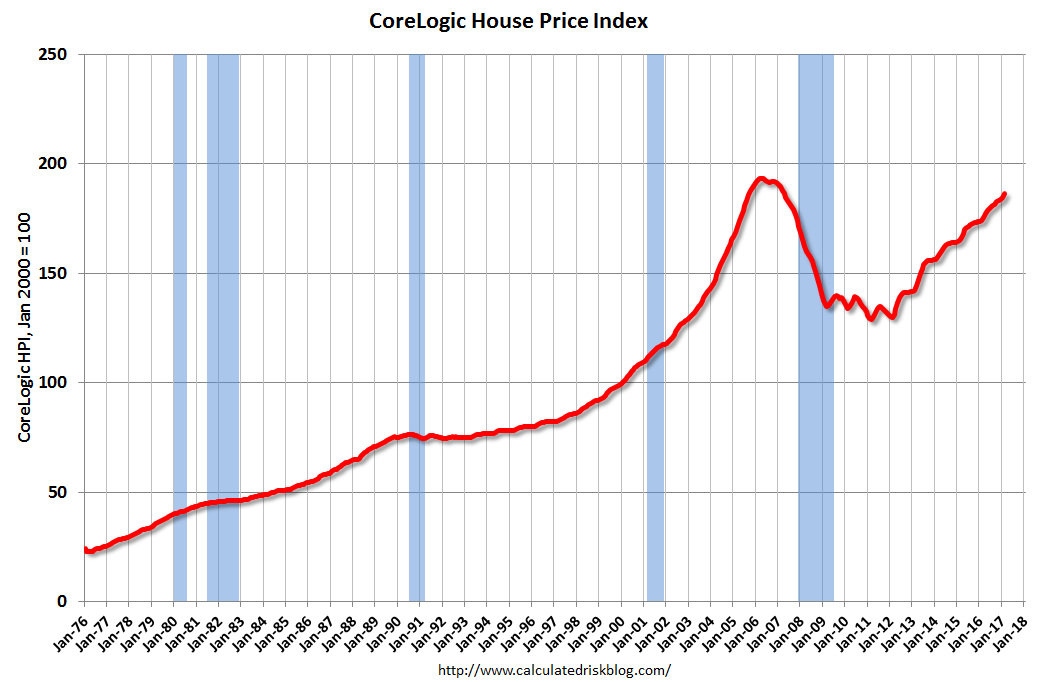

Click on graph for larger image.

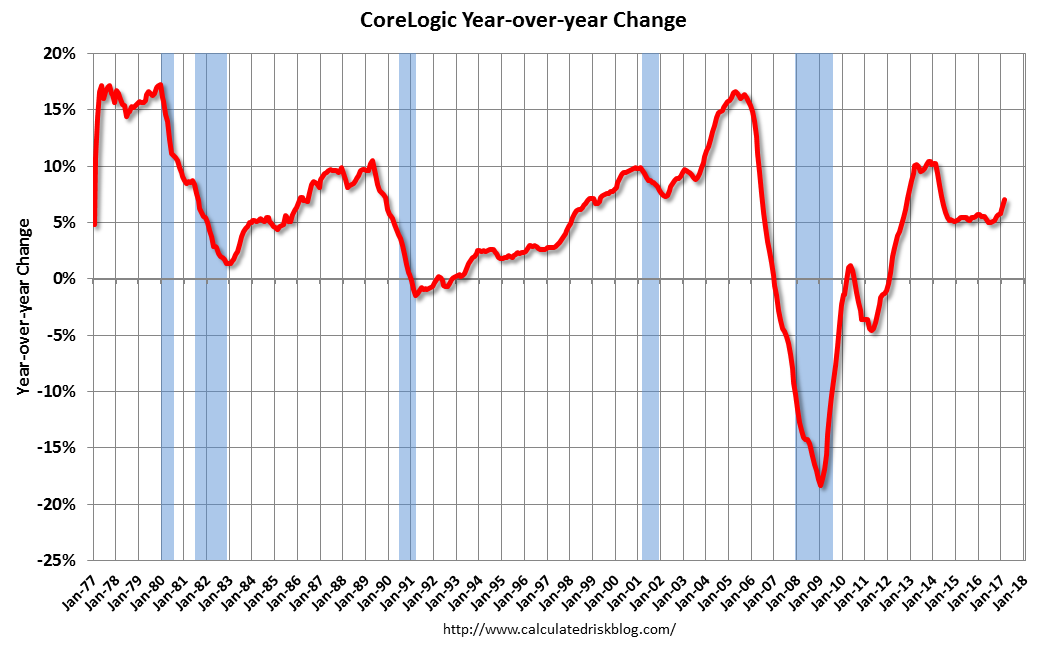

Click on graph for larger image.

This graph shows the national CoreLogic HPI data since 1976. January 2000 = 100.

The index was up 1.0% in February (NSA), and is up 7.0% over the last year.

This index is not seasonally adjusted, and this was another strong month-to-month increase.

The index is still 3.7% below the bubble peak in nominal terms (not inflation adjusted).

The second graph shows the YoY change in nominal terms (not adjusted for inflation).

The second graph shows the YoY change in nominal terms (not adjusted for inflation).

The YoY increase had been moving sideways over the last two years, but might have picked up recently (the recent pickup could be revised away).

The year-over-year comparison has been positive for five consecutive years since turning positive year-over-year in February 2012.