Black Knight Financial Services (BKFS) released their Mortgage Monitor report for March today. According to BKFS, 3.62% of mortgages were delinquent in March, down from 4.08% in March 2016. BKFS also reported that 0.88% of mortgages were in the foreclosure process, down from 1.25% a year ago.

This gives a total of 4.50% delinquent or in foreclosure.

Press Release: Black Knight’s March Mortgage Monitor: 19 Percent of Active HELOCs Are Scheduled to Reset in 2017

Today, the Data and Analytics division of Black Knight Financial Services, Inc. released its latest Mortgage Monitor Report, based on data as of the end of March 2017. This month, Black Knight took a closer look at home equity lines of credit (HELOCs), particularly on the share of HELOCs with draw periods – typically a 10-year term of interest-only payments before payments become fully amortizing – ending in 2017. Accounting for just under $100 billion in outstanding unpaid principal balances (UPB), these HELOCs represent the last of the pre-crisis lines of credit – those originated from between 2004 and 2007. As Black Knight Data & Analytics Executive Vice President Ben Graboske explained, as draw periods end and HELOCs reset with new payments, borrowers can face very different monthly obligations.

“In 2017, 19 percent of active HELOCs are facing reset,” said Graboske. “This is the largest share of active HELOCs facing reset of any single year on record, although the approximate 1.5 million borrowers slated to see their HELOC payments increase this year is about 100,000 fewer borrowers than in 2016. With the lines beginning to reset this year and early into 2018, we’re seeing the last of the pre-crisis-era HELOCs that the industry has been focusing on since early 2014. After deceleration in early 2018, we will have a lull of several years in reset activity. On average, borrowers facing resets this year are looking at a ‘payment shock’ of about $250 per month over their current HELOC payments – more than doubling their current payments, in fact. Historically, those increases have impacted HELOC performance significantly; delinquency rates of 2006 vintage HELOCs – which reset last year – jumped by 74 percent. That was marginally lower than the 2004 and 2005 vintages, which saw delinquency rates rise by 90 and 88 percent, respectively. Payment shocks remain high for lines resetting in 2018 but then drop along with the overall volume of resets in 2019.

“One thing that’s working in the 2007 vintage HELOCs’ favor has been the equity and interest rate environment of the last year. Rising home prices and low interest rates throughout 2016 have allowed borrowers to be much more proactive than in years past in terms of paying off or refinancing their lines to avoid increased monthly payments. For those still facing resets, however, equity continues to be a struggle. One-third of borrowers whose HELOCs will reset in 2017 have less than 20 percent equity in their home, making refinancing problematic. One in five have less than 10 percent, and one in 10 are actually underwater. Even that reflects improvement in home prices, though; last year 45 percent of borrowers facing reset had less than 20 percent equity and nearly 20 percent were underwater.”

emphasis added

Click on graph for larger image.

Click on graph for larger image.

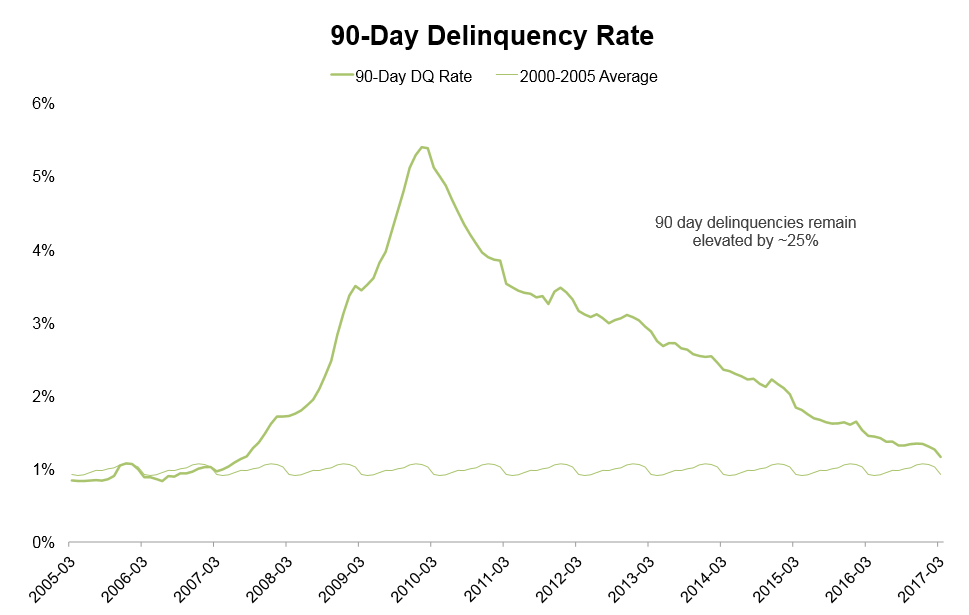

This graph from Black Knight shows the 90 day delinquency rate compared to the average of 2000 through 2005.

From Black Knight:

• Although the inventory of loans 90 or more days delinquent (but not yet in foreclosure) fell by 14 percent over Q1 2017 and is down 20 percent year-over-year, it remains roughly 25 percent above long term norms

• There are still over 250K more seriously delinquent (90+ days) and active foreclosure loans today than would be expected in a “healthy” market

• Approximately 40 percent of all delinquent mortgages are 30 days past due in today’s market; historically, that share has been closer to 55 percent, further reflecting the supply of lingering aged delinquencies

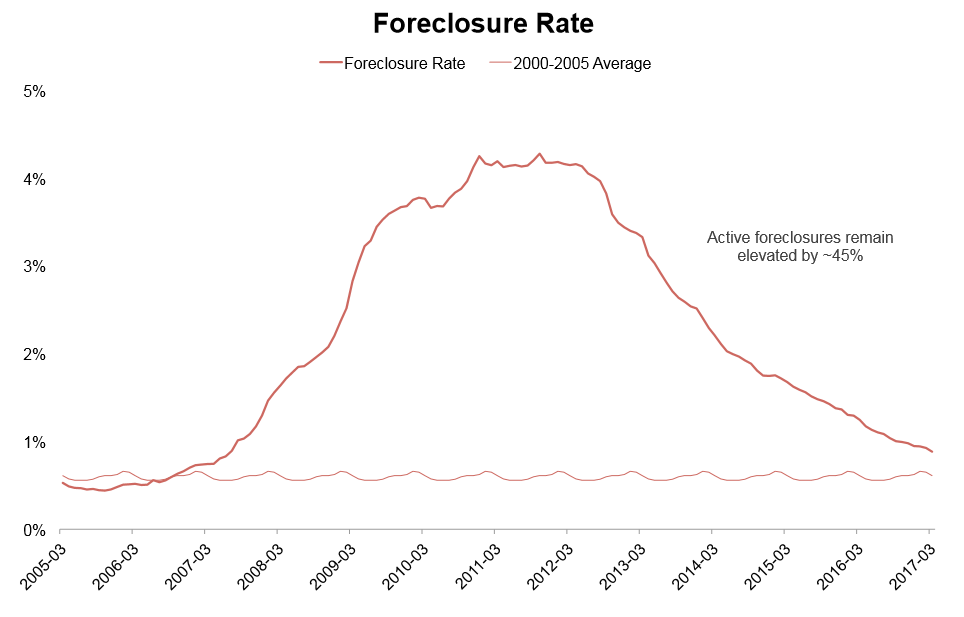

This graph from Black Knight shows the foreclosure rate compared to the 2000-2005 average,

This graph from Black Knight shows the foreclosure rate compared to the 2000-2005 average,

From Black Knight:

• Similarly, loans in the active foreclosure population have decreased by seven percent year-to-date and 29 percent year-over-year, but remain 45 percent above normal levels

• As 90+ day delinquent and active foreclosure inventories improve, overall delinquencies will continue to move toward a more normal distribution, albeit perhaps a lower than normal total volume of troubled loans

There is much more in the mortgage monitor.