On Friday, I posted five economic questions I’m frequently asked. I’ll post some thoughts on each of these topics over the next couple of weeks.

A common question is: Are house prices in a new bubble? My short answer was: No. Here is an explanation.

First, we need to define a bubble. Way back in April 2005, when I was very bearish on housing, I wrote: Housing: Speculation is the Key. From that post:

I have taken to calling the housing market a “bubble”. But how do I define a bubble?

A bubble requires both overvaluation based on fundamentals and speculation. It is natural to focus on an asset’s fundamental value, but the real key for detecting a bubble is speculation – the topic of this post. Speculation tends to chase appreciating assets, and then speculation begets more speculation, until finally, for some reason that will become obvious to all in hindsight, the “bubble” bursts.

First, on valuation: two key measures are house prices to income, and real house prices. The Census Bureau released the Income, Poverty and Health Insurance Coverage in the United States: 2016 in September. The report showed a significant increase in the real median household income:

The U.S. Census Bureau announced today that real median household income increased by 3.2 percent between 2015 and 2016 … Median household income in the United States in 2016 was $59,039, an increase in real terms of 3.2 percent from the 2015 median income of $57,230. This is the second consecutive annual increase in median household income.

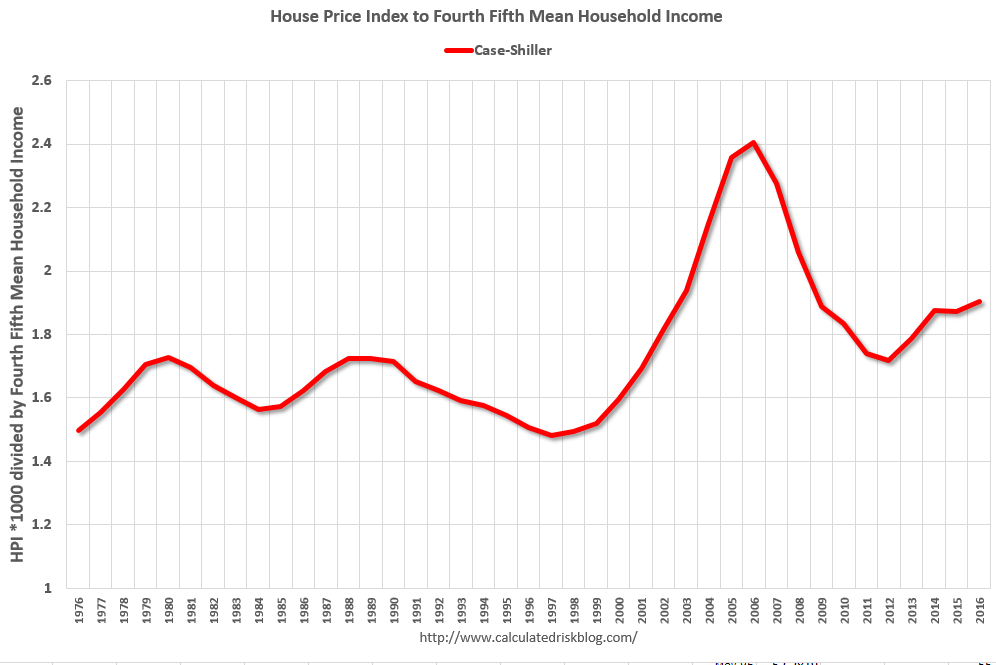

The firs two graphs use annual averages of the Case-Shiller house price index – and the nominal median household income (and the mean for the fourth fifth income) through 2016.

Click on graph for larger image.

Click on graph for larger image.

This graph shows the ratio of house price indexes divided by the Median Household Income through 2016 (the HPI is first multiplied by 1000).

This uses the annual average National Case-Shiller index since 1976.

As of 2016, house prices were above the median historical ratio – but far below the bubble peak.

The second graph is similar but uses the mean of the fourth fifth household income (if we separate households into fifths, this is the second highest income group).

These are key households since they are more likely to be homeowners (and home buyers).

These are key households since they are more likely to be homeowners (and home buyers).

Using this group, prices are well below the bubble peak.

By these measures, we could argue house prices are 15% to 20% too high, but this is a relatively small overvaluation compared to the 50%+ overpricing at the peak of the housing bubble.

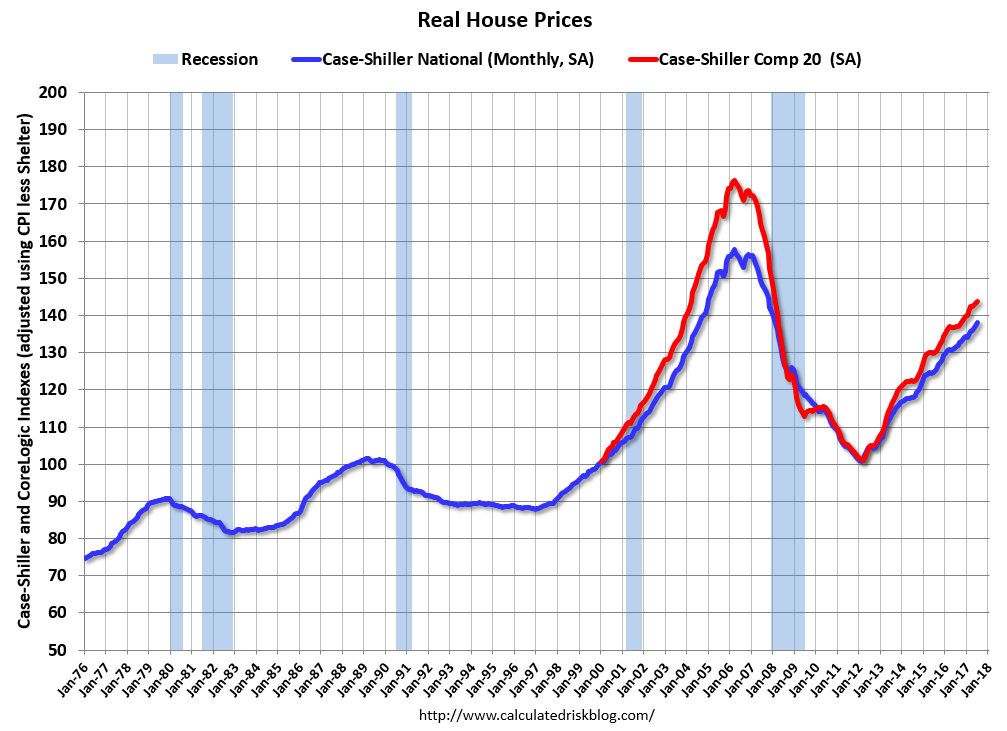

The third graph shows the monthly Case-Shiller National index SA, and the monthly Case-Shiller Composite 20 index SA (through July) in real terms (adjusted for inflation using CPI less Shelter). Note: some people use other inflation measures to adjust for real prices.

The third graph shows the monthly Case-Shiller National index SA, and the monthly Case-Shiller Composite 20 index SA (through July) in real terms (adjusted for inflation using CPI less Shelter). Note: some people use other inflation measures to adjust for real prices.

At first glance, this seems to suggest prices are 30% too high (and were maybe 50% to 60% too high during the bubble). However there is an upward slope to real prices, see The upward slope of Real House Prices and Lawler: On the upward trend in Real House Prices.

After adjusting for the historical upward slope in real prices, I’d estimate prices are about 15% too high.

On Speculation: Back in 2005, it was easy to identify excess speculation. There is currently some flipping activity, but this is more the normal type of flipping (buy, improve and then sell). Back in 2005, people were just buying homes are letting them sit vacant – and then selling without significant improvements. Classic speculation.

And even more dangerous during the bubble was the excessive use of leverage (all those poor quality loans). Currently lending standards are decent, and loan quality is excellent.

So prices may be a little overvalued, but there is little speculation – and I wouldn’t call house prices a bubble – and I don’t expect house prices to decline nationally like during the bust.