The key report this week is the October employment report on Friday.

Other key indicators include the October ISM manufacturing index, Personal Income and Outlays for September, and Case-Shiller house prices for August.

For manufacturing, the Dallas Fed manufacturing survey will be released this week.

The FOMC meets this week and is expected to lower rates 25bps.

8:30 AM ET: Chicago Fed National Activity Index for September. This is a composite index of other data.

10:30 AM: Dallas Fed Survey of Manufacturing Activity for September.

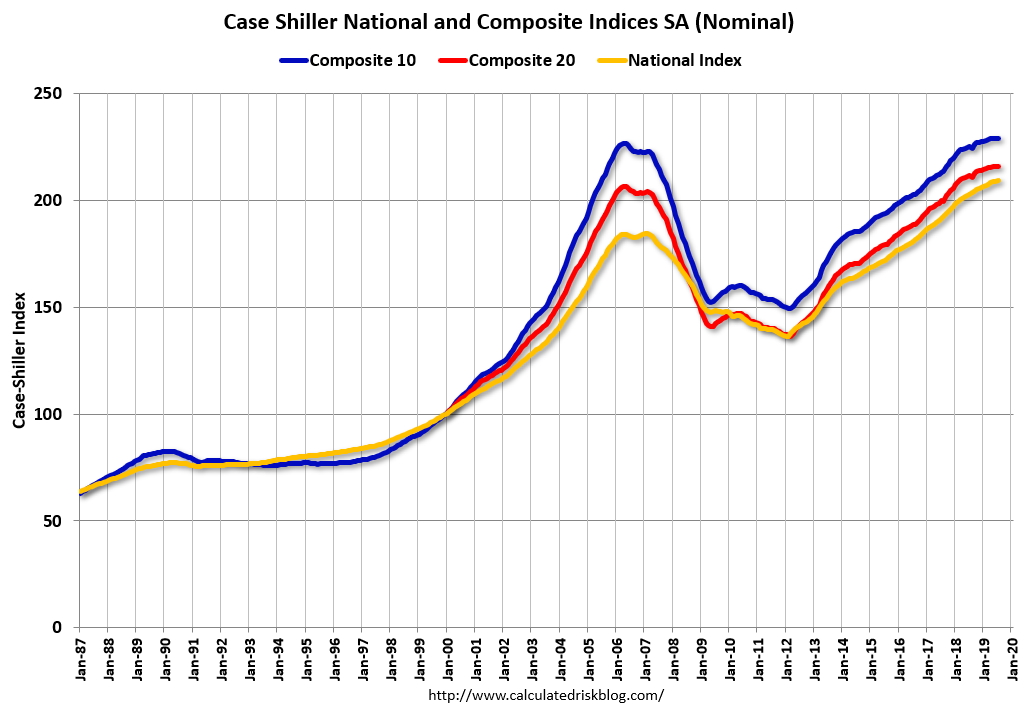

9:00 AM ET: S&P/Case-Shiller House Price Index for August.

9:00 AM ET: S&P/Case-Shiller House Price Index for August.

This graph shows the nominal seasonally adjusted National Index, Composite 10 and Composite 20 indexes through the most recent report (the Composite 20 was started in January 2000).

10:00 AM: Pending Home Sales Index for September. The consensus is 0.2% decrease in the index.

10:00 AM: The Q3 2019 Housing Vacancies and Homeownership report from the Census Bureau.

7:00 AM ET: The Mortgage Bankers Association (MBA) will release the results for the mortgage purchase applications index.

8:15 AM: The ADP Employment Report for October. This report is for private payrolls only (no government). The consensus is for 139,000 jobs added, up from 135,000 in September.

8:30 AM: Gross Domestic Product, 3rd quarter 2019 (advance estimate). The consensus is that real GDP increased 1.7% annualized in Q3, down from 2.0% in Q2.

2:00 PM: FOMC Meeting Announcement. The Fed is expected to lower the Fed Funds rate 25bps at this meeting..

2:30 PM: Fed Chair Jerome Powell holds a press briefing following the FOMC announcement.

8:30 AM: The initial weekly unemployment claims report will be released. The consensus is for 215,000 initial claims, up from 212,000 last week.

8:30 AM ET: Personal Income and Outlays for September. The consensus is for a 0.3% increase in personal income, and for a 0.2% increase in personal spending. And for the Core PCE price index to increase 0.1%.

9:45 AM: Chicago Purchasing Managers Index for October. The consensus is for a reading of 48.0, up from 47.1 in September.

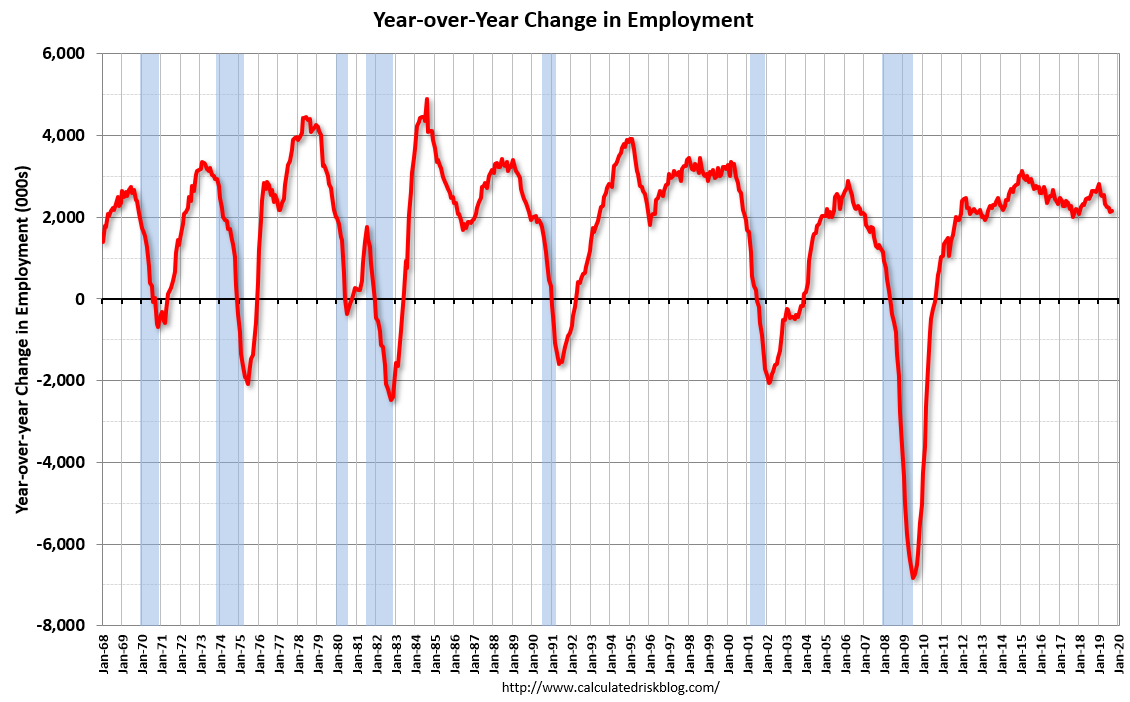

8:30 AM: Employment Report for October. The consensus is for 93,000 jobs added, and for the unemployment rate to increase to 3.6%.

8:30 AM: Employment Report for October. The consensus is for 93,000 jobs added, and for the unemployment rate to increase to 3.6%.

Note: The GM strike and supplier cutbacks (now settled) will probably subtract close to 75,000 jobs in October.

There were 136,000 jobs added in September, and the unemployment rate was at 3.5%.

This graph shows the year-over-year change in total non-farm employment since 1968.

In September, the year-over-year change was 2.147 million jobs.

A key will be the change in wages.

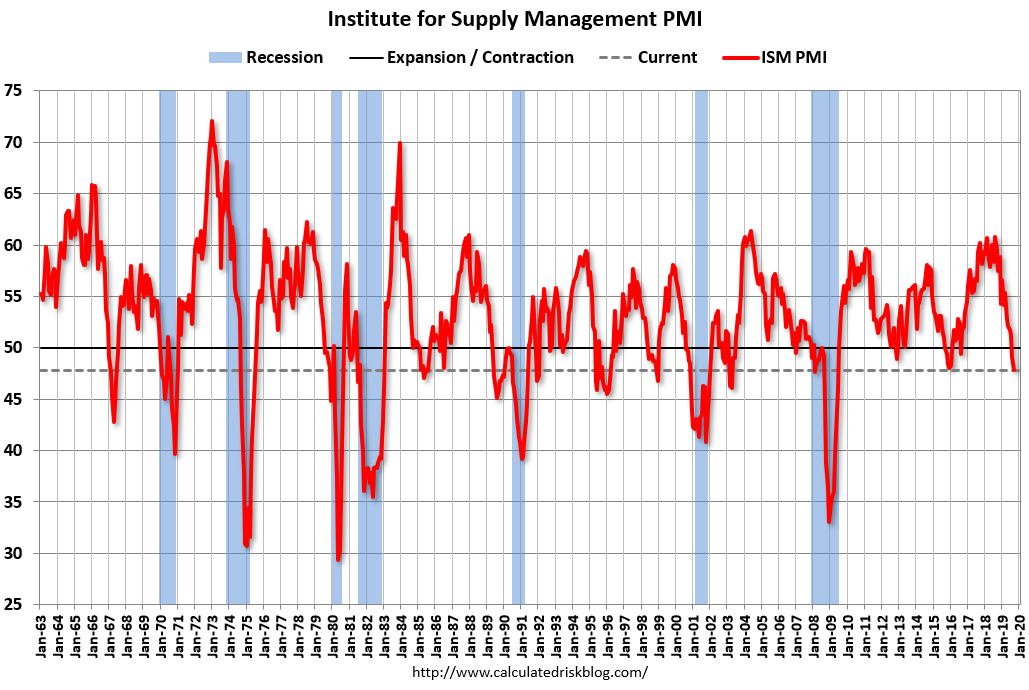

10:00 AM: ISM Manufacturing Index for October. The consensus is for 49.0%, up from 47.8%.

10:00 AM: ISM Manufacturing Index for October. The consensus is for 49.0%, up from 47.8%.

Here is a long term graph of the ISM manufacturing index.

The PMI was at 47.8% in September, the employment index was at 46.3%, and the new orders index was at 47.3%

10:00 AM: Construction Spending for September. The consensus is for 0.2% increase in spending.