The BEA has released the underlying details for the Q3 advance GDP report this morning.

The BEA reported that investment in non-residential structures decreased at a 14.6% annual pace in Q3. This is the fourth consecutive quarterly decline (weakness started before the pandemic).

Investment in petroleum and natural gas exploration decreased sharply in Q3 compared to Q2, and was down 60% year-over-year.

Click on graph for larger image.

Click on graph for larger image.

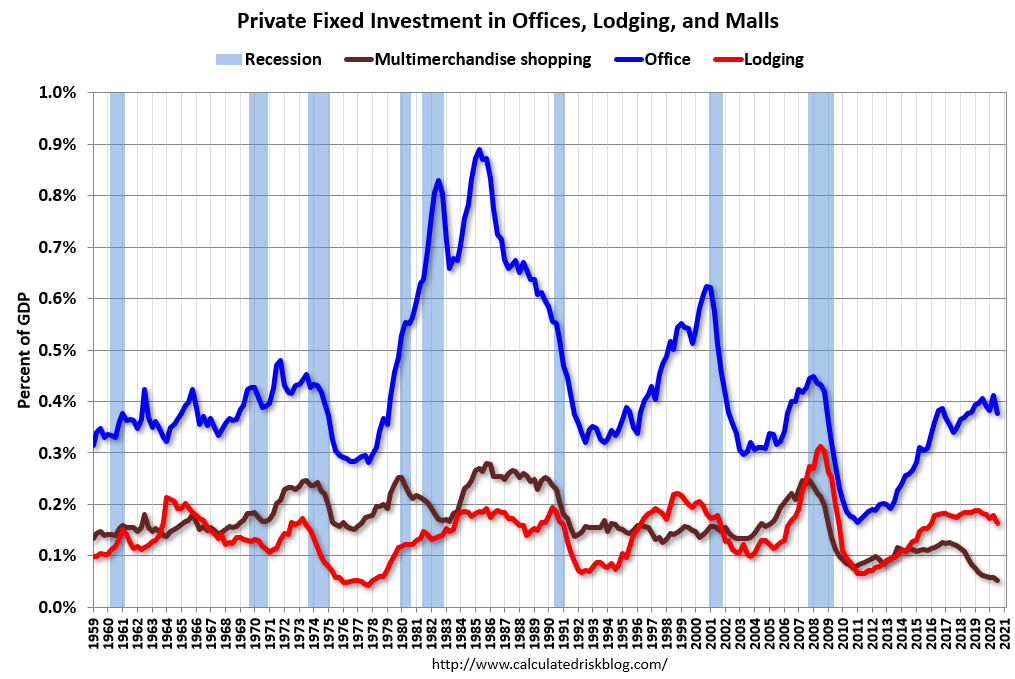

The first graph shows investment in offices, malls and lodging as a percent of GDP.

Investment in offices decreased in Q3, but was only down 5.9% year-over-year.

Investment in multimerchandise shopping structures (malls) peaked in 2007 and was down about 24% year-over-year in Q3 – and at a record low as a percent of GDP. The vacancy rate for malls is still very high, so investment will probably stay low for some time.

Lodging investment decreased in Q3, and lodging investment was down 14% year-over-year.

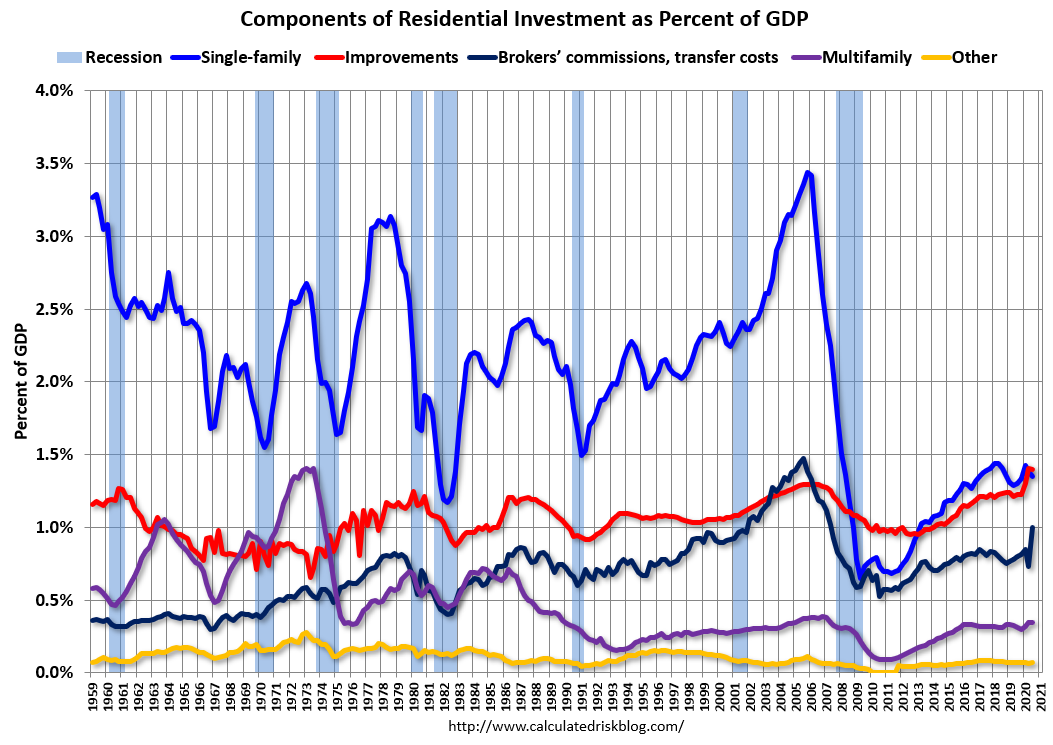

The second graph is for Residential investment components as a percent of GDP. According to the Bureau of Economic Analysis, RI includes new single family structures, multifamily structures, home improvement, Brokers’ commissions and other ownership transfer costs, and a few minor categories (dormitories, manufactured homes).

The second graph is for Residential investment components as a percent of GDP. According to the Bureau of Economic Analysis, RI includes new single family structures, multifamily structures, home improvement, Brokers’ commissions and other ownership transfer costs, and a few minor categories (dormitories, manufactured homes).

Even though investment in single family structures has increased from the bottom, single family investment is still low, and still below the bottom for previous recessions as a percent of GDP. I expect some further increases in single family investment.

Investment in single family structures was $285 billion (SAAR) (about 1.3% of GDP)..

Investment in multi-family structures increased in Q3.

Investment in home improvement was at a $296 billion Seasonally Adjusted Annual Rate (SAAR) in Q3 (about 1.4% of GDP). Home improvement spending has been solid and might hold up during the pandemic.