Note: This index is a leading indicator primarily for new Commercial Real Estate (CRE) investment.

From the AIA: Architecture Billings continue to lose ground

Demand for design services from U.S. architecture firms took a pointed dip last month, according to a new report from the American Institute of Architects (AIA).

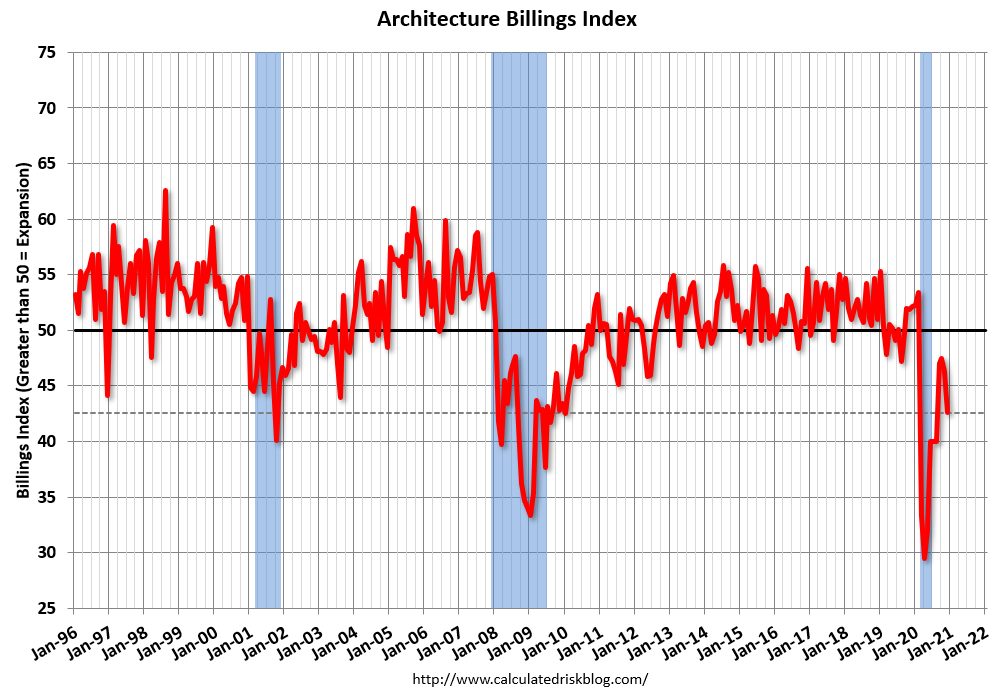

The pace of decline during December accelerated from November, posting an Architecture Billings Index (ABI) score of 42.6 from 46.3 (any score below 50 indicates a decline in firm billings). Meanwhile, the pace of growth of inquiries into new projects remained flat from November to December with a score of 52.4, though the value of new design contracts stayed in negative territory with a score of 48.5.

“Since the national economic recovery appears to have stalled, architecture firms are entering 2021 facing a continued sluggish design market,” said AIA Chief Economist Kermit Baker, PhD, Hon. AIA. “However, the recently passed federal stimulus funding should help shore up the economy in the short-term, and hopefully by later this year there should be relief as COVID vaccinations become more widespread. Recent project inquiries from prospective and former clients have been positive, suggesting that new work may begin picking up as we move into the spring and summer months.”

…

• Regional averages: South (46.8); Midwest (43.6); West (43.4); Northeast (38.8)• Sector index breakdown: mixed practice (48.0); commercial/industrial (47.2); multi-family residential (46.1); institutional (38.5)

emphasis added

Click on graph for larger image.

Click on graph for larger image.

This graph shows the Architecture Billings Index since 1996. The index was at 42.6 in December, down from 46.3 in November. Anything below 50 indicates contraction in demand for architects’ services.

Note: This includes commercial and industrial facilities like hotels and office buildings, multi-family residential, as well as schools, hospitals and other institutions.

This index has been below 50 for ten consecutive months. This represents a significant decrease in design services, and suggests a decline in CRE investment through most of 2021 (This usually leads CRE investment by 9 to 12 months).

This weakness is not surprising since certain segments of CRE are struggling, especially offices and retail.