I’ve been asked several times about the recent ECRI recession call (obviously I disagreed with their incorrect recession call in 2011 – I wasn’t even on recession watch then and I’m not on recession watch now – and I also think ECRI is wrong about a recession starting in mid-2012). Several people have written about ECRI’s call, see Menzie Chinn at Econbrowser, NDD at the Bonddad blog, and Henry Blodget at Business Insider.

It seems to me ECRI is trying to make this an academic exercise and hoping for some significant downward revisions. Right now the data doesn’t indicate a recession in 2012, but, as Menzie Chinn notes, “all of these series will be revised, so one wouldn’t want to state definitively we are not in a recession – therein lies the path to embarrassment. But the case still has to be made for recession.”

But why do we care? Here is a repeat of a post I wrote in early 2011 (with updated tables and charts):

From 2011 [updates in brackets]: Here is something very different. This is NOT intended as investment advice.

Why is there so much focus on the business cycle? For companies, especially cyclical companies, the reason is obvious – it helps with planning, staffing and investment. [Update: Most cyclical companies are expanding now]

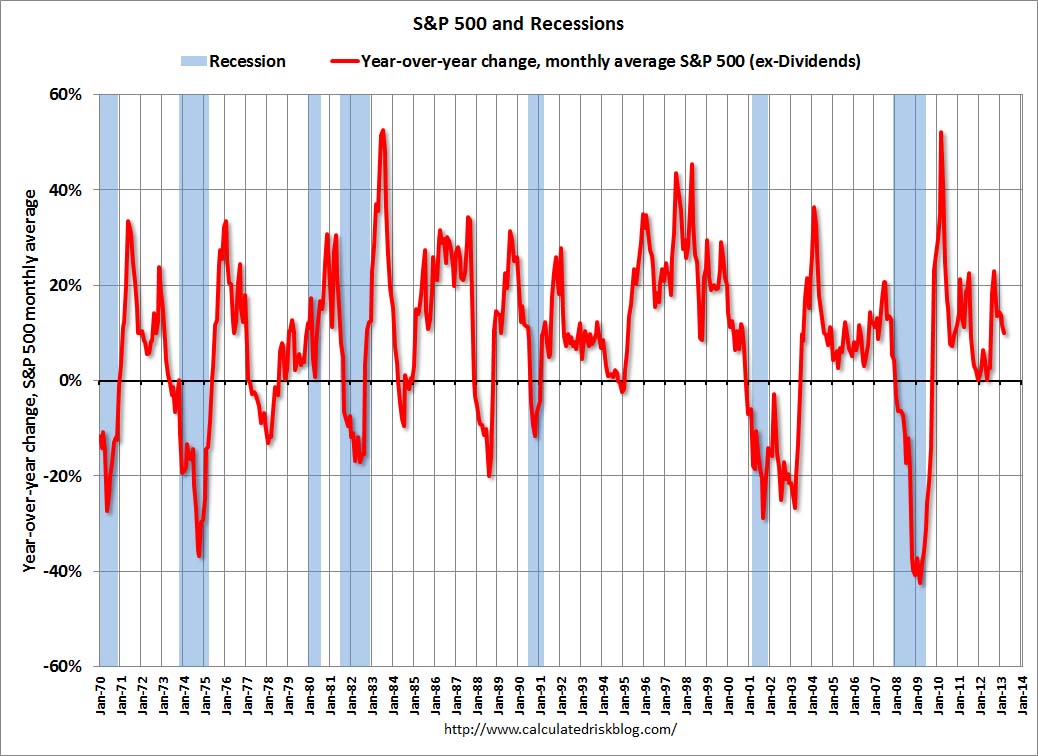

But why are investors so focused on the business cycle? Obviously earnings decline in a recession, and stock prices fall too. The following graph shows the year-over-year (YoY) change in the S&P 500 (using average monthly prices) since 1970. Notice that the market usually declines YoY in a recession.

Note: Because this is “year-over-year” there is a lag to the S&P 500 data. [Graph updated to March 2013]

Click on graph for larger image.

Click on graph for larger image.

So calling a recession isn’t just an academic exercise, there is some opportunity to preserve capital.

Not all downturns in the stock market are associated with recessions. As an example, the 1987 market crash was during an economic expansion. And the stock bubble collapse lasted from March 2000 through early 2003 – and the only official economic recession during that period was 7 months in 2001.

Although I don’t give investment advice, I think investors should measure their performance with some index. Warren Buffett likes to use the S&P 500 index, so I also used the S&P 500 for this exercise.

Imagine if we could call recessions in real time, and if we could predict recoveries in advance. The following table shows the performance of a buy-and-hold strategy (with dividend reinvestment), compared to a strategy of market timing based on 1) selling when a recession starts, and 2) buying 6 months before a recession ends.

For the buy and sell prices, I averaged the S&P 500 closing price for the entire month (no cherry picking price – just cherry picking the timing with 20/20 hindsight).

I assumed an investor started at four different times, in January of 1970, 1980, 1990, and 2000 [UPDATE: added 2010 start].

S&P 500 Annualized Return, including dividends |

||||||

|---|---|---|---|---|---|---|

| Return from Start Date | Recession Timing Sensitivity | |||||

| Start Investing | Buy and Hold | Recession Timing | Two Months Early | One Month Early | One Month Late | Two Months Late |

| Jan-70 | 8.92% | 13.09% | 12.15% | 12.81% | 13.01% | 12.46% |

| Jan-80 | 9.90% | 13.52% | 13.37% | 13.38% | 13.71% | 12.97% |

| Jan-90 | 7.80% | 12.30% | 11.91% | 12.20% | 12.23% | 11.65% |

| Jan-00 | 1.37% | 6.88% | 7.49% | 7.22% | 7.02% | 7.17% |

| Jan-10 | 11.18% | 11.18% | — | — | — | — |

The “recession timing” column gives the annualized return for each of the starting dates. Timing the recession correctly always outperforms buy-and-hold. The last four columns show the performance if the investor is two months early (both in and out), one month early, one month late, and two months late. The investor doesn’t have to be perfect!

Note: This includes dividends, but not taxes. Also I assumed no interest earned when the investor is out of the market (money in the mattress).

The second table provides the same information, but this time in dollars (assuming a $10,000 initial investment). Notice that someone could have bought the S&P 500 index in January 2000, and they’d be up about $150 [March 2013 Update: Up $1,970] now using buy-and-hold even though the market is still below the January 2000 average price of 1425 [Update: Now above January 2000]. The positive return is due to dividends.

S&P 500: Value of $10,000 Investment, including dividends |

||||||

|---|---|---|---|---|---|---|

| Value based on Start Date | Recession Timing Sensitivity | |||||

| Start Investing | Buy and Hold | Recession Timing | Two Months Early | One Month Early | One Month Late | Two Months Late |

| Jan-70 | $399,910 | $1,582,190 | $1,120,170 | $1,426,530 | $1,537,910 | $1,257,860 |

| Jan-80 | $228,630 | $520,810 | $499,670 | $500,540 | $549,080 | $447,700 |

| Jan-90 | $56,920 | $116,550 | $108,230 | $114,250 | $115,050 | $103,010 |

| Jan-00 | $11,970 | $21,020 | $22,400 | $21,770 | $21,330 | $21,680 |

| Jan-10 | $13,990 | $13,990 | — | — | — | — |

Unfortunately forecasters have a terrible record of predicting downturns. The running joke is that forecasters have predicted 9 of the last 5 recessions! Although a forecaster doesn’t have to be perfect, they still have to be right. And that is very rare.

As economist Victor Zarnowitz said way back in 1960: “The record of predicting turning points — changes in the direction of economic activity — is on the whole poor.” Forecasting hasn’t improved much since then.

As an example, here are some comments from then Fed Chairman Alan Greenspan in 1990 (a recession began in July 1990):

“In the very near term there’s little evidence that I can see to suggest the economy is tilting over [into recession].”

Chairman Greenspan, July 1990“…those who argue that we are already in a recession I think are reasonably certain to be wrong.”

Greenspan, August 1990“… the economy has not yet slipped into recession.”

Greenspan, October 1990

I’d say he missed that downturn. Of course Wall Street and Fed Chairmen are notoriously bad at calling downturns.

But the track record for calling recoveries isn’t much better. … Calling recessions is a mug’s game, but I like to play. I was very lucky with the recent recession, but the key wasn’t calling the end in June 2009 (I thought it ended in July), but looking for the bottom in early 2009 (that is why I posted several times in early 2009 that I was looking for the sun).

This is NOT intended as investment advice. I am NOT an investment advisor. Just some (hopefully) fun musing …

[Final Update: If investors sold when ECRI first made their recession call in Sept 2011, they would have a missed around a 30% increase in the market This shows why trying to add recession timing is difficult; investors have to be correct on the business cycle].