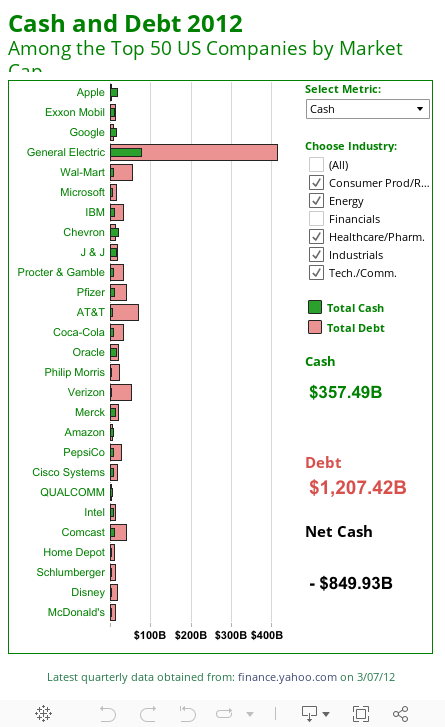

Here’s the question of the day: How much actual cash is on hand at corporations?

Fed by glowing reports from sell-side analysts, most investors are unaware that except for a handful of companies, there is no cash, only debt. Even counting short-term investments there is surprisingly little cash on hand.

Courtesy of Mike Klaczynski at Tableau Software please consider the latest update to my periodic “Cash Cow” interactive report.

The data for this sheet is from Yahoo!Finance. Scroll over any of the bars (not the company name) to see more details.

Cash is a liability not an asset for banks, so I left off financial

corporations in the default map. Certainly the $277 billion in cash on

hand at Bank of America is not a sign of genuine strength or

profitability.

As you can see, actual cash on hand at non-financial corporations is a net negative $850 billion.

Five Cash Cows With Genuine Cash

- Apple (AAPL) $16.15 Billion

- Chevron (CVX) $8.03 Billion

- Google (GOOG) $7.57 Billion

- Qualcomm (QCOM) $4.26 Billion

- Amazon (AMZN) $3.70 Billion

The grand total of actual available cash (at the five companies that have any) is $15.53 billion.

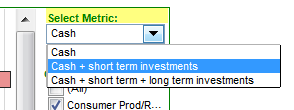

To add in short-term investments, click on the Select Metric drop-box that looks like this:

Here are the results.

10 Cash Cows Counting Short-Term Investments

- Microsoft (MSFT) $54.09 Billion

- Google (GOOG) $40.88 Billion

- Apple (AAPL) $39.82 Billion

- Cisco (CSCO) $30.09 Billion

- Oracle (ORCL) 13.94 Billion

- Qualcomm (QCOM) $13.24 Billion

- Chevron (CVX) $8.30 Billion

- Amazon (AMZN) $7.07 Billion

- Intel (INTC) $4.59 Billion

- Johnson & Johnson (JNJ) $4.03 billion

Net Negative Cash

Counting short-term investments, net corporate cash of the 50 largest companies is negative $543.67 billion.

Total cash of the 10 companies that have positive balance sheet cash (counting short-term investments as a cash equivalent) is $216.05 billion.

This is a far cry from the $trillions in sideline cash we are told is ready to come pouring into the market any time now. The facts of the matter are:

- Sideline cash is a direct function of debt

- Sideline cash cannot come into the market to propel shares higher because for every buyer of a security there is a seller, except for debt offerings and IPOs

Yet, the concept of “sideline cash” as widely believed and highly touted by mainstream media is mathematically impossible.

It is possible however, for a corporation to use its

cash to buy back shares, but in that case, sideline cash will be

transferred to another account (frequently the cash account of an

insider who is bailing).

Recall that investors wanted Apple to buy back shares last Autumn, thinking they were undervalued at $700. Today’s price is $435.

Had Apple been foolish enough to buy back shares when everyone seemed convinced the next stop was $1000, Apple’s share price would undoubtedly be lower today, reflective of the amount of cash it wasted on buybacks.

2009 and 2010 provided excellent opportunities for corporations to buy back shares. Bargains have long since vanished.

Mike “Mish” Shedlock

http://globaleconomicanalysis.blogspot.com